For decades, European entrepreneurs have faced a complex challenge: launching a business across the EU meant navigating 27 different national legal systems and more than 60 company types. A California startup could expand to all 50 US states under one legal framework. A European startup needed entirely separate corporate entities for each country. Consider the reality, A Berlin-based SaaS company with a dream to expand across Europe faced this roadblock. They were incorporated in Germany, then had to establish separate subsidiaries in France, Italy, Spain, Poland, and the Netherlands. Each incorporation required local legal counsel, unique compliance documentation, and separate tax filings. Annual costs climbed into six figures just to maintain corporate structures that weren’t directly generating revenue.

That inefficiency shaped European business for generations. It created a competitive disadvantage against American companies with unified legal structures. It consumed entrepreneurial energy on compliance rather than product development.

That era is ending.

On 18 March 2026, the European Commission formally proposed EU Inc., officially known as Societas Europaea Unificata (S.EU) or the “28th regime”. This is a single, optional, pan-European company structure that allows any business to incorporate and operate across all 27 EU member states under one harmonised legal framework. The proposal has already attracted powerful backing: 22,000+ signatories, including Europe’s leading founders, investors, and startup communities, have endorsed the vision. This level of grassroots support, combined with formal EU Commission backing, signals serious momentum toward adoption by late 2026.

What makes this different from previous failed attempts? The EU Commission learned from the mistakes of the Societas Europaea (SE), a similar structure proposed in 2001 that saw minimal adoption. EU Inc. removes the barriers that killed the SE: minimum capital requirements, complex governance rules, and member-state discretion, which created cross-border variation.

What Is EU Inc.?

EU Inc. is a fundamentally new legal category for European business. Unlike national company forms (like Ireland’s Ltd or Germany’s GmbH), EU Inc. isn’t registered in any single member state. Instead, it’s registered in a unified EU-level registry.

Core Definition

EU Inc. (Societas Europaea Unificata) is an optional, pan-European company form that allows any business, regardless of size, sector, or founder nationality, to incorporate and operate across all 27 EU member states under harmonised rules.

Why “Optional”?

This is crucial: EU Inc. doesn’t replace existing national structures. Businesses can choose to use it alongside (not instead of) traditional company forms, like:

- UK Ltd

- German GmbH

- Irish Ltd

- Estonian OÜ

- Spanish SL

Historical Context: The Failed SE

To understand why EU Inc. matters, look at its predecessor: the Societas Europaea (SE), created in 2001.

The SE was supposed to solve the same problem. Instead, it became a cautionary tale:

- €120,000 minimum capital requirement: created friction for startups

- Complex governance rules: each EU member state added its own discretionary requirements

- High legal costs: the complexity defeated the purpose

- Poor adoption rates: only 2,000+ SEs exist across the entire EU (vs. millions of national companies)

EU Inc. was designed to fix all three failures.

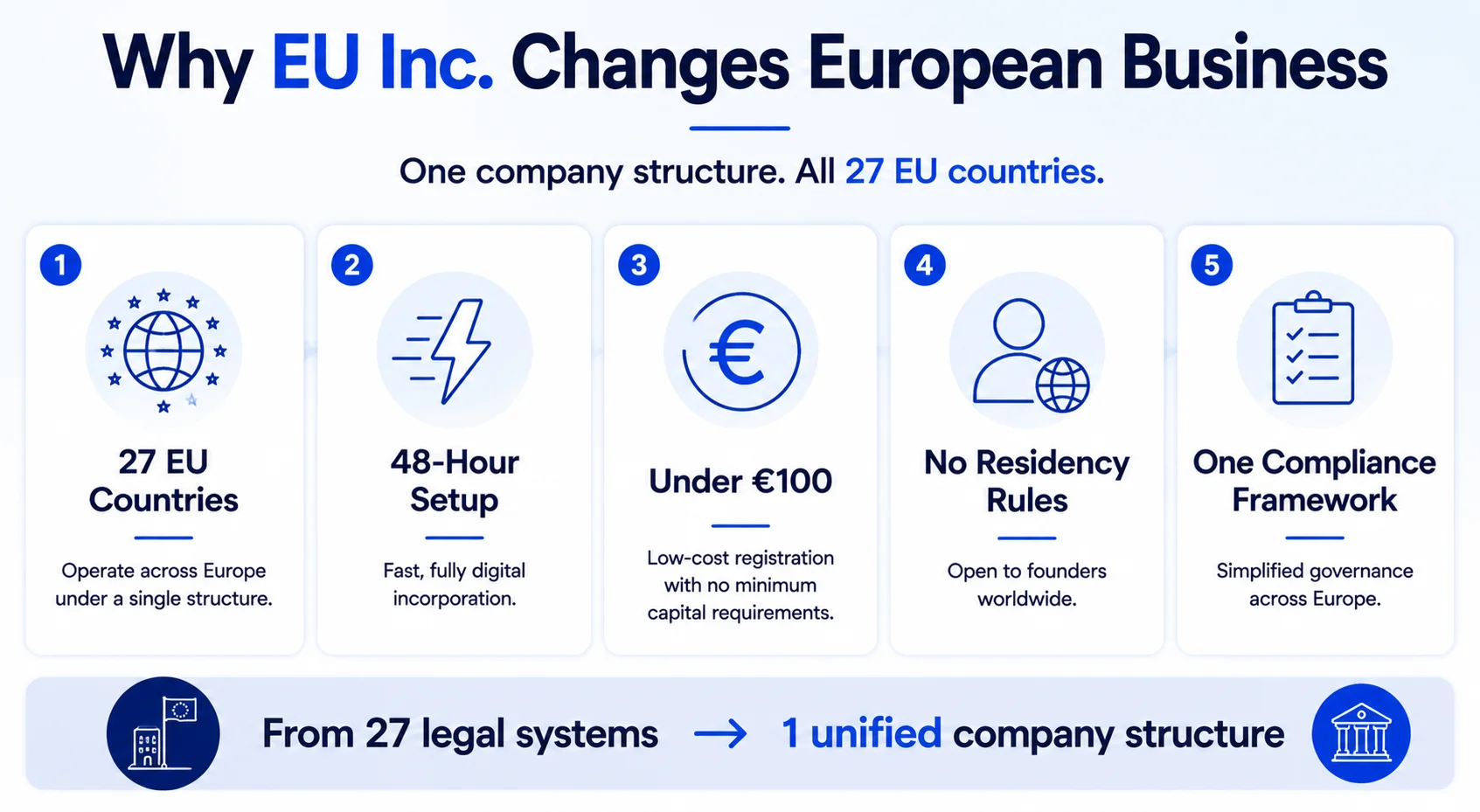

Key Features of EU Inc.: What Makes It Different

1. Incorporation in 48 Hours: Fully Digital, Anywhere

- You can incorporate an EU Inc. company in 48 hours, entirely online, from anywhere in the world.

- No physical presence required. No lengthy administrative processes. No waiting for government offices.

2. Less Than €100 to Set Up

- No minimum share capital requirement, unlike traditional SEs or many national structures.

- This removes a significant barrier for startups and founders with limited initial capital.

3. One Central EU-Level Registry

- EU Inc. companies register in a single, harmonised registry, not in a specific member state.

- This eliminates multiple registrations, multiple legal filings, and the cost of coordinating across national authorities.

4. Unified Rules Across All 27 EU Member States

A single set of rules for:

- Corporate governance

- Incorporation procedures

- Investment and capital management

- Dissolution and liquidation

No more navigating 27 different legal systems.

5. Accessible to Any Business

- Whether you’re a one-person freelancer, a 50-person scaleup, or a 500-person SME, EU Inc. is available to you.

- No sector restrictions (though banking and insurance face additional EU and national rules regardless of legal form).

6. Non-EU Founders Welcome

- No residency requirement. Non-EU citizens and companies from the UK, US, Asia, or elsewhere can establish EU Inc. companies.

- This opens European markets to international founders without forcing them to relocate or use complex nominee structures.

7. EU-FAST Investment Instrument

- Alongside EU Inc., the Commission proposed EU-FAST, a standardised investment vehicle for venture funding.

- This companion structure simplifies cap table management and investor agreements across borders.

8. Operates Alongside National Forms

- EU Inc. doesn’t force a migration. Businesses can maintain national subsidiaries while using EU Inc. as their main operating entity.

- This flexibility matters for companies with complex, multi-jurisdictional structures.

What Problem Does EU Inc. Actually Solve?

The Fragmentation Tax: Real Costs for Real Businesses

Today, European expansion looks like this for most startups:

| Stage | Reality |

|---|---|

| Year 1 | Incorporate in Ireland or the Netherlands |

| Year 2-3 | Open subsidiaries in Germany, France, and Spain as you expand |

| Year 4-5 | Add Poland, Italy, and Belgium to serve the growing customer base |

| Ongoing | Maintain separate financial reporting, tax compliance, and governance for each entity |

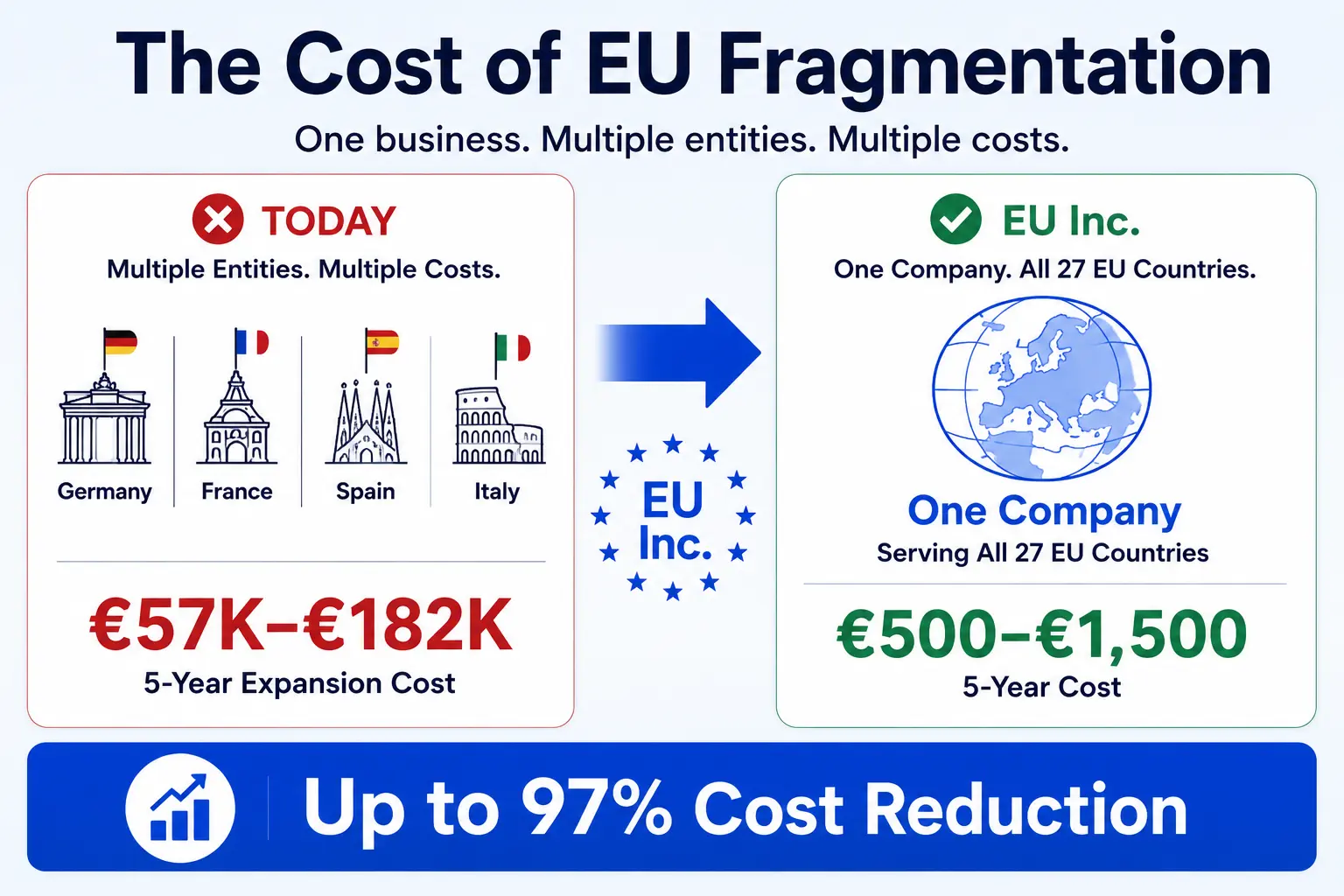

Cost breakdown for a typical scale-up (5 EU country expansion):

- Legal fees for each incorporation: €1,500–€5,000 per country × 5 = €7,500–€25,000

- Annual compliance costs per subsidiary: €800–€2,500 per year × 5 entities × 5 years = €20,000–€62,500

- Accounting and tax specialists: Managing 27 different VAT systems, 5 different tax regimes = €15,000–€40,000 annually

- Governance overhead: Separate boards, shareholder meetings, regulatory filings for each entity = €10,000–€30,000 annually

- Currency management and inter-company transfers: Managing cash flow across entities and currencies = €5,000–€15,000 annually

- Time cost: Founder and operations team managing compliance across 5 jurisdictions = Immeasurable but significant

Total 5-year cost for expanding to 5 EU countries: €57,500–€182,500

For early-stage startups operating on thin margins, this fragmentation tax isn’t trivial. For mid-market companies, it’s a hidden drag on profitability that competitors in the US don’t face.

EU Inc. collapses this to:

- Single incorporation: €50–€100

- Single annual compliance filing to the EU registry

- One VAT number, one EU tax return (with country breakdowns)

- One cap table, one governance structure

- Unified banking and treasury management

- No inter-company complexity

Total 5-year cost with EU Inc.: €500–€1,500

Savings: €56,000–€181,000 a 97% reduction in legal and compliance overhead

Case Study: How EU Inc. Changes the Game for Real Companies

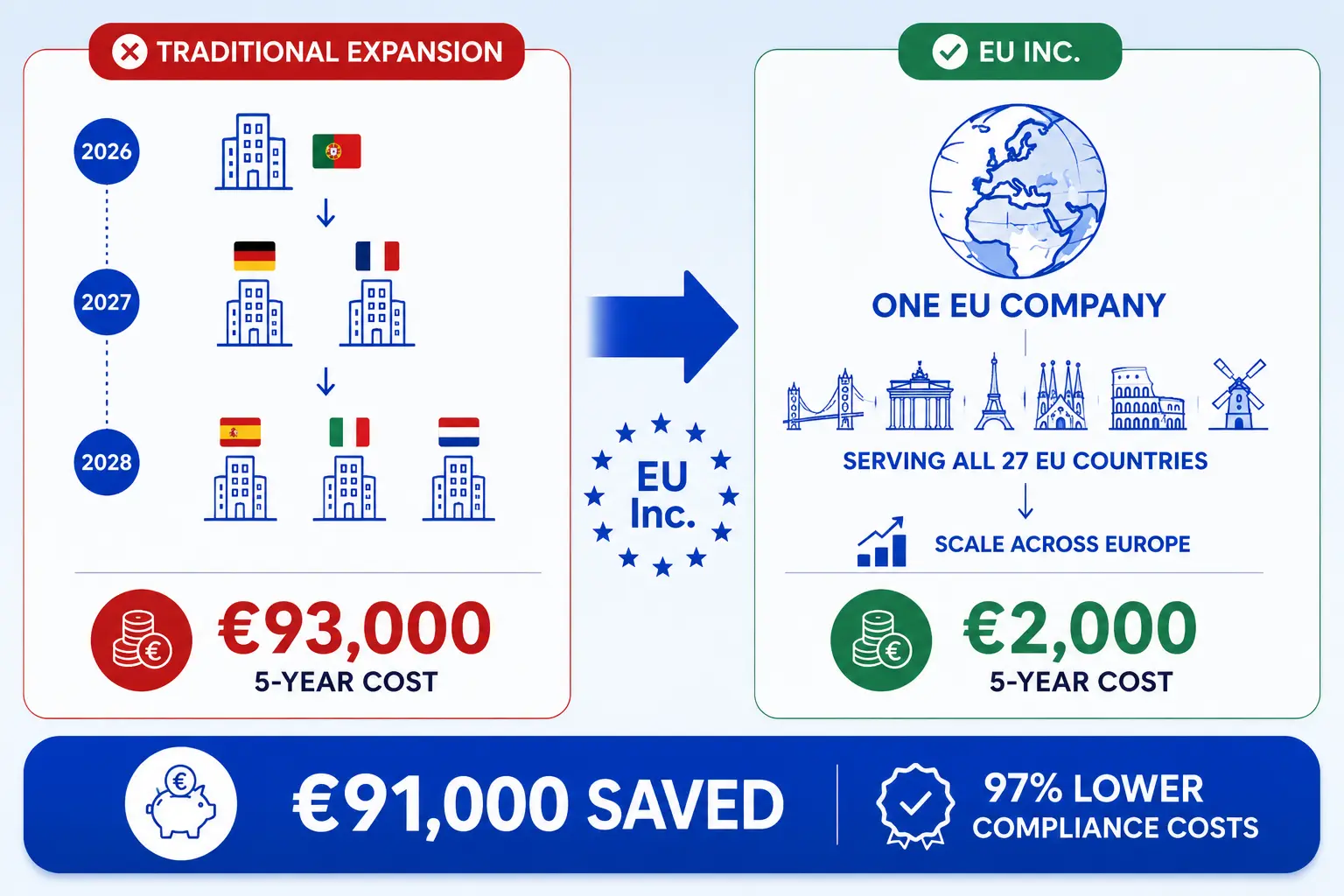

Imagine FinTech Europa, a Portuguese fintech startup founded in 2026 with a strong product-market fit in Portugal.

Scenario A: Using current structures (Ireland Ltd + subsidiaries)

- Incorporates in Ireland (Day 1) Cost: €400

- Year 2: Expands to Germany and France (customer demand) Cost: €3,000 (2 subsidiaries @ €1,500 each)

- Year 3: Expands to Spain, Italy, Netherlands (Series A investor requirement for EU scale) Cost: €4,500 (3 subsidiaries @ €1,500)

- Years 1–5: Annual compliance across 6 entities. Cost: €60,000 (6 entities × €2,000 annually × 5 years)

- Hiring specialized accountant familiar with multi-country tax costs: €25,000

- Total 5-year cost: ~€93,000

- Management complexity: Finance team spends significant time on inter-company transfers, currency management, separate tax filings

- Fundraising impact: Series A investors request a clean-up and restructuring before closing additional legal fees of €10,000–€20,000

Scenario B: Waiting for EU Inc. (launch 2027)

- Incorporated the EU Inc. company in 2027. Cost: €80

- Operates legally across all 27 EU states from Day 1

- Serves German, French, Spanish, Italian customers from the same legal entity

- No additional incorporation needed as market expands

- Years 2–5: Single annual compliance filing to EU registry Cost: €2,000 (€400 × 5 years)

- One in-house finance person manages all compliance no specialist needed

- Total 5-year cost: ~€2,000

- Management simplicity: Finance team focuses on strategy, not inter-company logistics

- Fundraising advantage: Clean, modern EU-native structure ready for growth, no restructuring needed before Series A

- Flexibility: Can serve all 27 EU states immediately without future incorporation overhead

Tangible savings with EU Inc.: ~€91,000 (97% reduction in legal/compliance costs)

This is the real transformation EU Inc. enables.

The Competitive Disadvantage EU Inc. Eliminates

A US startup raises capital in Silicon Valley, expands to all 50 US states under one Delaware C-Corp structure, maintains a single board, and keeps one set of books. Legal infrastructure is essentially invisible to the operations team founders focus on product and growth.

A European startup, until now, faces a structurally different reality:

- Expand across multiple countries? Must incorporate separate subsidiaries in each (expensive, complex, diverts bandwidth from product)

- Stay concentrated in one country? Limits addressable market and growth trajectory

- Use complex holding structures? Requires expensive legal advice, ongoing management, and creates investor skepticism

This structural disadvantage has contributed to the documented “European entrepreneurship gap,” the observation that European startups often lag American peers in scale, growth rates, and exit valuations, even when they have equally strong technology and markets.

Research from venture capital analysts suggests that founder time spent on compliance and legal complexity (rather than product development) is a material drag on European company growth rates.

EU Inc. finally eliminates this structural disadvantage.

Economic Impact (European Commission Estimates)

The official proposal includes ambitious but grounded economic projections:

Direct estimates:

- 300,000 new companies expected in the first decade

- 1.6 million new jobs created through new business formation and geographic expansion

- €35 billion+ in reduced compliance costs across the EU economy over a 10-year period

- 15–20% increase in cross-border business activity among EU companies

Underlying logic:

If EU Inc. enables 300,000 companies that wouldn’t otherwise form due to fragmentation barriers, and those companies employ an average of 5–6 people each, the job creation math is straightforward. More importantly, if existing European companies can expand more cost-effectively across borders:

- Larger, more competitive European champions emerge to compete globally with American and Chinese incumbents

- Innovation clusters distributed across Europe (not concentrated in Dublin, Amsterdam, London, or Berlin)

- Venture capital and startup activity spread more evenly reducing brain drain from smaller EU economies (Poland, Portugal, Greece, etc.)

- European tech ecosystems develop more geographic resilience

Who Is EU Inc. Designed For?

Ideal Use Cases (With Real Examples)

Startups and Scaleups Expanding Across Multiple EU Markets

If you’re growing from Germany to France to Spain (a common trajectory for European SaaS companies), EU Inc. lets you do that under one legal entity instead of incorporating three separate subsidiaries.

Example: A Berlin-based HR tech startup with customers in 5 EU countries can operate under a single EU Inc. entity instead of maintaining separate GmbHs in Germany, France, Spain, Italy, and Netherlands. This eliminates at least €10,000 in annual compliance costs.

Non-EU Companies (UK, US, Asia) Seeking EU Entry

American, British, or Asian founders no longer need:

- A local EU partner to hold the operating company

- Complex subsidiary structures

- Nominee directors in each country

Simply incorporate an EU Inc. company directly from the US, Singapore, or anywhere else in the world.

Example: A San Francisco SaaS company expanding to Europe doesn’t need to hire a legal entity manager in Dublin or Amsterdam. They can register an EU Inc., open a bank account, and start serving customers immediately.

Venture-Backed Companies Managing Complex Cap Tables

EU Inc. includes standardized investor protections and a companion investment instrument (EU-FAST), making fundraising across borders much simpler than managing different shareholder structures across multiple national entities.

Example: A startup raising a Series A from investors across Europe, US, and Asia can use a single EU Inc. cap table instead of converting from Irish Ltd to SE to EU Inc. across multiple funding rounds.

SMEs and Mid-Market Companies Streamlining Cross-Border Operations

A manufacturing company based in Poland serving customers in 8 EU countries currently maintains:

- Polish parent company

- German, Czech, Slovak, Austrian, Hungarian subsidiaries

- Separate tax filings in each jurisdiction

- Currency complexity across 4+ different countries

EU Inc. consolidates this to one legal entity, one tax return, one set of books.

Impact: One CFO can now manage what previously required 2–3 compliance specialists.

Existing Companies Converting from National to EU Structure

Once EU Inc. becomes available, established companies can migrate from national structures (Irish Ltd, German GmbH) to EU Inc. if the economics make sense particularly if they:

- Have expanded to 4+ EU countries

- Are planning further geographic growth

- Want to simplify cap tables ahead of fundraising

- Are dealing with high annual compliance costs

Who Should Wait (For Now)

Single-Country Operations

If you’re operating in one EU country (Germany, France, Spain) and genuinely have no plans to expand across borders, your national company form (Irish Ltd, German GmbH, Estonian OÜ) remains simpler and more cost-effective. There’s no benefit to using EU Inc. if you’ll never operate in more than one jurisdiction.

Highly Regulated Sectors with National Oversight

Banking, insurance, pharmaceuticals, and similar industries face additional EU and national regulations regardless of legal form.

- A German bank opening under EU Inc. still needs German banking regulator approval

- An insurance company operating across Europe still needs authorization from regulators in each country where it operates

- Pharmaceutical companies still need EMA approval plus national registrations

EU Inc. doesn’t simplify these compliance requirements. If you’re in a heavily regulated sector, consult with regulatory counsel before deciding on EU Inc.

Companies with Existing Complex Structures

If you already have a sophisticated holding structure with operations across multiple countries, the cost of converting to EU Inc. might exceed the annual savings, particularly if your current structure includes intellectual property holding companies, pension funds, or other specialized vehicles.

This requires case-by-case analysis with your tax advisors.

Legislative Timeline: When Will EU Inc. Actually Be Available?

What’s Happened So Far

| Date | Event |

|---|---|

| January 2026 | EU Commission President Ursula von der Leyen announces EU Inc. vision at World Economic Forum in Davos; EU-INC movement reaches 22,000+ signatories |

| 18 March 2026 | European Commission publishes formal legislative proposal (COM(2026) 321) |

| 19 March 2026 | European Council Conclusions officially support expedited adoption |

What’s Coming

| Phase | Timeline | Details |

|---|---|---|

| Ordinary Legislative Procedure | 2026 (ongoing) | European Parliament and Council of 27 member states negotiate final text |

| Adoption Target | End 2026 | Strong political will to complete formal adoption by year-end |

| Implementation | 2027 | EU Inc. available for actual company registrations |

Why the Speed Is Realistic

The legal basis for EU Inc. is Article 114 TFEU (harmonisation of internal market rules), which allows approval by qualified majority voting, not unanimity.

This is critical: unlike some EU regulations requiring all 27 member states to agree, EU Inc. only needs approximately 72% of the weighted vote. This significantly accelerates the process.

Compare this to the SE, which required unanimity and took years to negotiate.

How EU Inc. Compares to Existing Options

If you’re considering EU market entry today, here’s how EU Inc. stacks up against other popular choices:

| Feature | EU Inc. (2027) | Ireland Ltd | UK Ltd | US LLC | Estonian OÜ |

|---|---|---|---|---|---|

| Registration Time | 48 hours | 5–10 days | 24 hours | 1–5 days (varies) | 1–3 days |

| Cost | <€100 | €300–€500 | £40–£300 | $100–$500 | €100–€200 |

| Min. Capital | None | None | None | None | None |

| EU-Wide Operation | Yes (single entity) | Yes (with subsidiaries) | Limited (post-Brexit) | Limited | Yes (with subsidiaries) |

| Digital Incorporation | Full | Mostly | Yes | Varies | Yes |

| Non-EU Founders | Yes | Yes | Yes | Yes | Yes |

| Investor Protections | Standardised (EU-FAST) | Irish law | UK law | State-dependent | Estonian law |

| Annual Compliance | Single EU filing | Ireland only | UK only | Varies by state | Estonia only |

When to Choose What (Until 2027)

Choose Ireland Ltd if:

- You need EU operations now

- You’re planning significant investor fundraising

- You want a known, established legal framework

Choose Estonian OÜ if:

- You’re a solopreneur or early-stage startup

- You want speed and low cost

- You value digital-first operations

Wait for EU Inc. if:

- You’re not scaling until 2027 or later

- You plan multi-country EU operations

- You want to minimize future restructuring

What the Critics Are Saying (And Why It Matters)

EU Inc. hasn’t escaped scrutiny. Understanding the concerns and the Commission’s responses helps you assess whether this structure is right for you.

Concern 1: Employee Rights and Worker Participation

- Criticism: The European Trade Union Confederation (ETUC) and worker advocates argue that employee protections and works council requirements are insufficient in the proposal.

- What They’re Asking For: Stronger mandatory worker participation and board representation requirements in EU Inc. governance.

- Commission Response: EU Inc. is designed alongside the broader “Savings and Investments Union” strategy, which includes labour market protections. The framework isn’t a race to the bottom but a harmonisation toward high standards.

- Likely Outcome: The final regulation will likely include enhanced worker protections before adoption.

Concern 2: Speed vs. Scrutiny

- Criticism: Corporate Europe Observatory and civil society groups worry that 48-hour registration could enable shell companies and reduce tax authority oversight.

- What They’re Asking For: Longer registration periods and more identity verification.

- Commission Response: 48-hour registration will include mandatory beneficial ownership registration and compliance with EU anti-money laundering directives. Speed ≠ lack of scrutiny.

- Likely Outcome: The final framework will include robust AML/KYC requirements, making fast registration compatible with proper oversight.

Our Assessment

The proposal will likely be modified during negotiations, particularly on worker protections and due diligence requirements. However, the core structure is sound and will survive the legislative process.

Businesses should prepare now by understanding the outline, so you’re not surprised when the final rules arrive.

What Should Businesses Do Right Now? A Practical Action Plan

You have several options depending on your timeline and EU expansion strategy. Rather than vague advice, here’s a concrete action plan for each situation.

Option 1: Incorporate in an Established EU Jurisdiction Now (2026)

Best for

Companies needing operations immediately, raising capital in 2026–2027, or planning single-country operations.

Top choices

Ireland Ltd

- Registration time: 5–10 days

- Cost: €300–€500

- Advantages: Largest EU tech hub, English-speaking legal/accounting resources, familiar to all investors, strong IP protection laws

- Best for: Companies raising from VCs, planning significant growth, wanting established legal framework

- Compliance: Manageable single entity with strong professional services ecosystem

Estonia OÜ

- Registration time: 1–3 days (fully digital)

- Cost: €100–€200

- Advantages: Most digital incorporation experience globally, lowest cost, modern legal framework, strong non-EU founder experience

- Best for: Bootstrapped founders, solopreneurs, tech-first operations, non-EU founders wanting simplicity

- Compliance: Exceptional digital-first systems, minimal paperwork

Netherlands BV

- Registration time: 5–10 days

- Cost: €500–€800

- Advantages: Strong intellectual property protections, favorable tax treaty network, strong for tech/IP companies

- Best for: Companies with significant IP, planning global expansion beyond EU, needing specialized tax planning

- Compliance: Complex but highly sophisticated professional services available

Option 2: Wait for EU Inc. (2027)

Best for

Companies whose expansion timeline extends into 2027+, bootstrapped founders, or those planning 4+ country EU operations.

Implementation timeline

| Month | Action |

|---|---|

| Now (May 2026) | Begin market research and customer development in target EU countries using your current home country entity |

| Q3 2026 | Monitor EU Commission’s legislative progress; engage with EU Inc. advisors to understand final framework |

| Q4 2026 | Final regulation should be adopted; prepare incorporation documentation and banking setup |

| Q1 2027 | EU Inc. becomes available for registration → incorporate immediately |

| Q2 2027 | Begin EU operations under unified EU Inc. structure |

Key advantage

You avoid duplicate work and incorporation costs. Single, clean structure from day one of EU operations.

Option 3: Hybrid Approach (Recommended for Most Scaleups)

Incorporate in Ireland or Estonia now, migrate to EU Inc. in 2027

Implementation

| Timeline | Action | Cost |

|---|---|---|

| Q2 2026 | Incorporate Ireland Ltd or Estonia OÜ to serve immediate market | €400–€500 |

| Q2–Q4 2026 | Begin generating EU revenue under this entity | Ongoing |

| Q4 2026 | EU Inc. regulation adopted; understand final framework | €0 |

| Q1 2027 | Evaluate migration: Is annual savings > migration cost? | Depends |

| Q1–Q2 2027 | If yes, migrate to EU Inc. (€2,000–€5,000 legal fees); if no, continue current structure | €2,000–€5,000 or €0 |

This approach

Gives you operational flexibility (move fast if needed) while maintaining strategic optionality (migrate to EU Inc. if it makes sense).

Immediate Action Items (What to Do This Month)

Now

- Define your EU timeline: Not “eventually,” actual month/quarter for first EU revenue

- Map your geographic expansion: Which EU countries first? 1–2 or 4+?

- Review your fundraising timeline: Will you raise capital before or after EU Inc. availability?

- Engage advisors: Email your accountant/lawyer with this question: “Should we wait for EU Inc. or incorporate in Ireland/Estonia now?”

Q3 2026

- Subscribe to EU Inc. updates at EU Inc. Official Portal and EU-INC Movement

- Watch Parliament and Council negotiations: get a sense of how framework is solidifying

- If you chose “wait,” finalize market research: in target EU countries (identify customers, understand regulations, gauge demand)

Q4 2026

- Finalize your EU structure decision: once regulation is adopted (should be clear by October 2026)

- If incorporating now, execute quickly: Q4 is good time for administrative work

- If waiting for EU Inc., prepare incorporation documents: (business plan, cap table, banking documents, beneficial ownership info)

Comparative Analysis: EU Inc. vs. All Alternatives

This expanded comparison helps you see exactly what you gain and lose with each option:

| Feature | EU Inc. (2027) | Ireland Ltd | UK Ltd | US LLC | Estonian OÜ |

|---|---|---|---|---|---|

| Registration Time | 48 hours | 5–10 days | 24 hours | 1–5 days | 1–3 days |

| Cost | <€100 | €300–€500 | £40–£300 | $100–$500 | €100–€200 |

| Min. Capital | None | None | None | None | None |

| EU-Wide Operation | Yes (single entity) | Yes (requires subsidiaries) | Limited (post-Brexit) | Limited (requires subsidiaries) | Yes (requires subsidiaries) |

| Digital Incorporation | Full | Partial | Yes | Varies | Full |

| Non-EU Founders | Yes | Yes | Yes | Yes | Yes |

| Annual Compliance Cost | €300–€500 | €1,500–€3,000 | €1,000–€2,500 | $500–$2,000 | €400–€800 |

| 5-Country Expansion Cost (5 years) | €2,000 | €35,000–€65,000 | €25,000–€50,000 | €20,000–€45,000 | €10,000–€20,000 |

| Investor Familiarity | Growing (2027+) | Established | Declining | Strong | Growing |

| Tax Efficiency | EU-harmonized | Ireland-optimized | UK-based | US-optimized | Estonia-optimized |

| Regulatory Complexity | Single regime | Single regime | Single regime | Single regime | Single regime |

Key insight

For pan-EU operations (4+ countries), EU Inc. is dramatically cheaper and simpler. For single-country operations, national forms remain more appropriate.

Understanding why the SE didn’t work helps explain why EU Inc. was necessary.

The SE Problem: A Cautionary Tale

The Societas Europaea was created under the 2001 SE Regulation with high hopes. Two decades later:

- Only ~2,500 SE companies exist across the entire EU

- Adoption remains concentrated in large, multinational corporations

- Startups and SMEs rarely use the form

Why?

| Problem | SE Reality | EU Inc. Solution |

|---|---|---|

| Minimum Capital | €120,000 required | Zero required |

| National Discretion | Member states added conflicting requirements | Harmonised rules across all 27 states |

| Cost | €5,000–€15,000+ in legal fees | <€100 |

| Governance Complexity | Multiple compliance regimes depending on where directors sit | Single, unified governance framework |

| Registration Speed | 4–8 weeks | 48 hours |

The SE was designed with large, multinational corporations in mind. EU Inc. is designed for the next generation: startups, scaleups, and SMEs.

Key Considerations Before You Choose Your EU Structure

Before deciding whether to wait for EU Inc. or incorporate now, evaluate these factors using a decision-making framework:

Factor 1: Timeline to Revenue

| Situation | Recommendation | Rationale |

|---|---|---|

| Generating revenue in 2026 | Incorporate now (Ireland, Estonia, Netherlands) | You need operational structure immediately; waiting 6-12 months is not viable |

| Targeting Q1-Q2 2027 launch | Consider waiting OR incorporate now + migrate later | Depends on how close you are to EU Inc. availability; risk vs. certainty trade-off |

| Targeting Q3-Q4 2027+ launch | Wait for EU Inc. | Timeline aligns with EU Inc. availability; avoid incorporation costs entirely |

Factor 2: Geographic Scope

| Scope | Current Cost | EU Inc. Benefit |

|---|---|---|

| Single EU country | €400–€500 for one incorporation | No benefit use national form |

| 2–3 EU countries | €1,500–€3,000 (1 main + 1–2 subsidiaries) | Marginal benefit Ireland Ltd still works |

| 4–6 EU countries | €5,000–€10,000 (1 main + 3–5 subsidiaries) | Moderate benefit EU Inc. saves €4,000–€8,000 annually |

| 7+ EU countries or pan-EU | €10,000–€20,000 (1 main + 6+ subsidiaries) | High benefit EU Inc. saves €8,000–€15,000 annually |

Factor 3: Investor Requirements

Institutional Fundraising Before 2027?

Your investors (especially institutional VCs) may have specific requirements:

- Some require Delaware C-Corp equivalents (Ireland Ltd is the European standard)

- Some are comfortable with any EU structure

- EU-based family offices and angels increasingly interested in EU-native structures

If you’re raising from Silicon Valley VCs in 2026, they’ll likely request an Ireland Ltd or Dutch BV. EU-based investors might be more flexible.

Bootstrapped or Later-Stage Rounds (2027+)?

If your next fundraising happens after EU Inc. is available (late 2027 or later), using EU Inc. signals:

- Strategic thinking about European operations

- Modern approach to cross-border structure

- Efficiency-focused operations (lower compliance overhead = higher profitability)

Savvy investors will appreciate the setup.

Factor 4: Operational Complexity

High operational complexity across multiple jurisdictions?

Manufacturing with supply chains in Germany, Hungary, and Czechia, EU Inc. dramatically simplifies:

- One contract with suppliers (all under same entity)

- Single insurance policy across all operations

- Unified treasury management

- One bank account for all operations

Simple digital operations with distributed team?

If you’re a fully remote SaaS company serving EU customers, the operational simplification is still valuable but less dramatic than a physically distributed operation.

Real-World Decision Scenarios: What Should YOU Do?

Scenario 1: Early-Stage Startup, Revenue in 6 Months

Your situation

You’ve raised €100k seed round, product is nearly ready, have initial customers lined up across 3 EU countries.

Decision

Incorporate in Ireland or Estonia now (2026)

Rationale

- You need operational structure immediately to invoice customers and process payments

- Waiting 6–12 months for EU Inc. risks revenue and customer relationships

- Cost of Ireland/Estonia incorporation (€400–€500) is trivial compared to revenue at stake

- Once EU Inc. is available (2027), you can evaluate migration if economics make sense

Timeline

Incorporate this month → start revenue → evaluate EU Inc. migration in Q4 2027 once framework is finalized

Scenario 2: Growth-Stage Scaleup, Series A in Q1 2027

Your situation

€2M ARR, operating in 5 EU countries, raising Series A in Q1 2027.

Decision

Act immediately with dual-track approach

Rationale

- You currently have 5 separate entities (likely costing €15,000–€25,000 annually in compliance)

- Series A investors will want clean structure before closing (likely requesting consolidation)

- Consolidating to EU Inc. after it launches (late 2027) would create 3-month delays post-fundraising

Timeline

- Q4 2026: Consolidate 5 entities into one Ireland Ltd holding company (€5,000–€10,000 in legal fees)

- Q1 2027: Clean structure ready for Series A closing

- Q4 2027: Evaluate migration to EU Inc. if economics favorable (one-time €3,000–€5,000 migration cost vs. €10,000+ annual savings)

Scenario 3: Bootstrapped Founder, No Revenue Yet, Expanding to EU in 2027

Your situation

Profitable business in Portugal, expanding to EU market in 2027, no outside investors yet.

Decision

Wait for EU Inc. (2027)

Rationale

- You don’t need capital structure (no investors) so no pressure to use investor-familiar structures

- Timeline allows waiting for EU Inc. availability

- Zero minimum capital requirement of EU Inc. aligns with bootstrapped approach

- €80 incorporation cost is far cheaper than €500 for Ireland Ltd

- Avoid duplicate work: one incorporation instead of Portugal + Ireland + EU Inc.

Timeline

- Q4 2026: Finalize product, prepare for launch

- Q1 2027: EU Inc. becomes available → incorporate

- Q2 2027: Begin EU expansion under unified EU Inc. structure

Scenario 4: Non-EU Founder, US-Based, Entering EU Market

Your situation

San Francisco SaaS company, €5M ARR in US, ready to expand to 4–5 EU countries.

Decision

Wait for EU Inc. if possible; if customer momentum requires immediate presence, incorporate Ireland Ltd now.

Rationale

- As a US company, EU Inc. is particularly valuable: no need for local EU nominee or partner

- If the timeline allows, waiting means avoiding Ireland Ltd incorporation entirely

- If customer demand is urgent, Ireland Ltd + future migration to EU Inc. still makes sense (Ireland Ltd can operate alongside EU Inc., or can be wound down)

Timeline

- If expansion can wait 6–12 months: Wait for EU Inc., incorporate late 2027

- If expansion is needed now: Incorporate Ireland Ltd immediately, migrate to EU Inc. in late 2027 when costs are known

Extending Your Thinking: Long-Term Strategic Implications

Beyond the immediate incorporation decision, EU Inc. affects longer-term planning:

- If you’re bootstrapped or planning to stay independent, EU Inc.’s low cost and full EU coverage is a game-changer for eventual multi-country operations.

- If you’re venture-backed, EU Inc. likely becomes the default structure for Series B+ (late 2027 onward) as it becomes the established market standard.

- If you’re acquiring other EU companies, EU Inc. simplifies post-acquisition integration (consolidates into a single parent entity rather than managing a subsidiary network).

- If you’re planning an exit/acquisition: Potential acquirers (especially European or Asian buyers) will appreciate a clean EU Inc. structure vs. complicated subsidiary networks.

Conclusion: EU Inc. as a Strategic Inflection Point

EU Inc. represents the most significant reform to European company law in decades. The combination of formal Commission backing, overwhelming founder and investor support (22,000+ signatories), and the legal mechanism for expedited adoption (qualified majority voting) makes this genuinely different from failed past attempts.

The strategic question isn’t whether EU Inc. will happen; it will. The question is how it affects your European expansion timeline.

Whether you act now with a national incorporation or wait strategically for EU Inc., you should understand the landscape. The businesses that move intentionally rather than reactively will have the advantage.