The EU’s 6th Anti-Money Laundering Directive (6AMLD) requires all EU member states to transpose updated beneficial ownership register rules into national law by 10 July 2026 – and enforcement has never been more serious.

Anyone operating through a nominee director, holding shares in a complex ownership chain, or incorporating a company anywhere in the EU now faces stricter disclosure rules, tighter deadlines, and a new access regime shaped by the landmark 2022 CJEU court ruling. Penalties range from €500 for minor breaches to €1,000,000 in Germany for serious violations. Banks are refusing to open accounts for companies without verified UBO registration. And the EU’s new Anti-Money Laundering Authority (AMLA) is beginning cross-border supervisory activity from 2026/2027 – meaning the patchwork of enforcement that let some companies slip through is closing fast.

The Panama Papers leak of 2016 was the turning point that made global governments take beneficial ownership transparency seriously. It revealed how complex, multi-layered ownership structures spanning multiple offshore jurisdictions could be used to conceal the identities of individuals controlling vast sums, while appearing entirely legal on the surface. The EU’s AML directive programme, from the 4th through to the 6th, is a direct legislative response to that moment and the systemic vulnerabilities it exposed.

This guide answers the questions most compliance teams and business owners are asking right now: Who exactly is a UBO? What must be registered? Who can see it? And what does 6AMLD actually change? Whether you are a corporate services provider, an in-house compliance officer, or a business owner using nominee arrangements, this guide covers everything you need to act before the July 2026 deadline.

What Is a Beneficial Owner (UBO)?

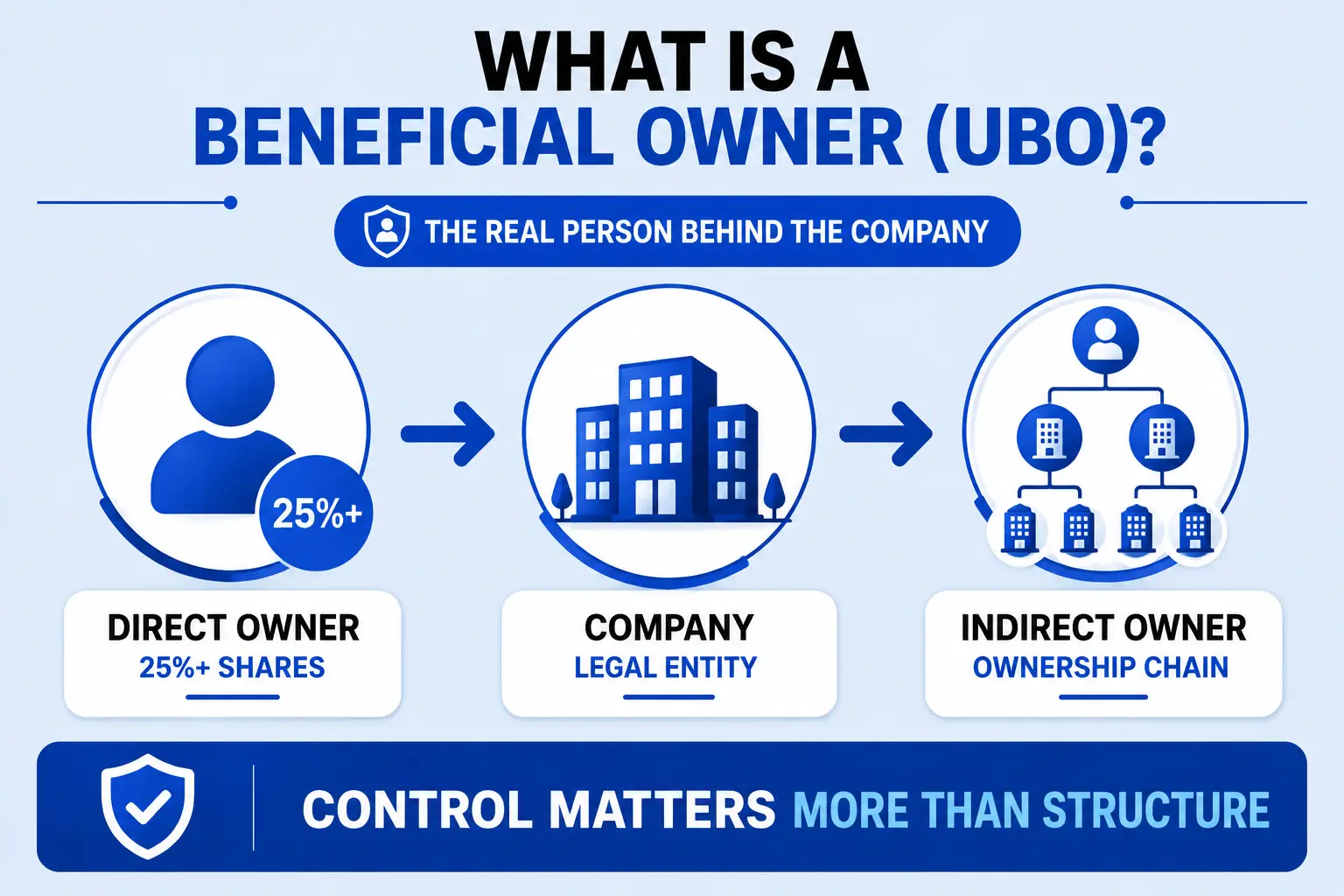

Under EU law, an ultimate beneficial owner (UBO) is the natural person who ultimately owns or controls a legal entity – whether through direct shareholding, indirect ownership chains, or other means of control.

A UBO is always an individual human being, never another company or legal entity. The chain of ownership must be traced all the way to a real person. This principle – that you must look through corporate layers until you reach an actual individual – is the foundation of the entire UBO framework.

The standard EU threshold is 25%. Any individual who holds 25% or more of shares, voting rights, or other ownership interests in a company is classified as a UBO.

Direct vs. Indirect Ownership – How the Calculation Works

The distinction between direct and indirect ownership is central to UBO compliance, and is where most companies make errors.

- Direct ownership is straightforward: the individual holds shares or voting rights in the company itself.

- Indirect ownership involves control exercised through one or more intermediate companies. The ownership percentage is calculated by multiplying holdings at each level of the chain.

Example: Person A owns 60% of Company B. Company B owns 60% of Company C. Person A’s indirect ownership of Company C is 60% x 60% = 36% – above the 25% threshold. Person A is therefore a UBO of Company C, even though they have no direct relationship with it whatsoever.

This calculation must be applied to the entire ownership chain, no matter how many layers it contains. A common compliance failure is stopping the analysis at the first legal entity rather than tracing all the way to the ultimate individual. Groups with holding companies, sub-holdings, and operating subsidiaries across multiple jurisdictions must map the entire structure – not just each entity in isolation.

What Counts as “Control” Beyond Shareholding?

The 25% ownership threshold is not the only route to UBO status. “Control” under EU AML law is deliberately broad. It also includes:

- Rights to appoint or remove board members or senior management

- Veto rights over significant corporate decisions

- Influence exercised through shareholder agreements or contractual arrangements

- Control through family ties or personal relationships not reflected in the share register

- Rights to the majority of profits, even without a controlling share

Under 6AMLD, a second trigger applies independently of ownership percentage: the “person with ultimate influence” – anyone who can exercise decisive influence over a legal entity, regardless of their stake. This is particularly relevant in structures where a founder retains operational control without holding a significant share, or where a financier controls decisions through loan covenants or board representation rights.

The Fallback Rule: Senior Managing Official

What if no individual meets the 25% threshold? The fallback rule applies: the senior managing official – typically the CEO or Managing Director – is registered as the UBO. This is a compliance mechanism, not an exemption. It signals to regulators that no beneficial owner above the threshold has been identified, which itself triggers additional scrutiny in some jurisdictions. Regulators treat the fallback registration as a flag, not a clean bill of health.

Some higher-risk sectors may apply a lower 15% threshold with European Commission approval under 6AMLD – particularly in industries assessed as carrying elevated money laundering risk, such as real estate, virtual asset services, and high-value goods trading.

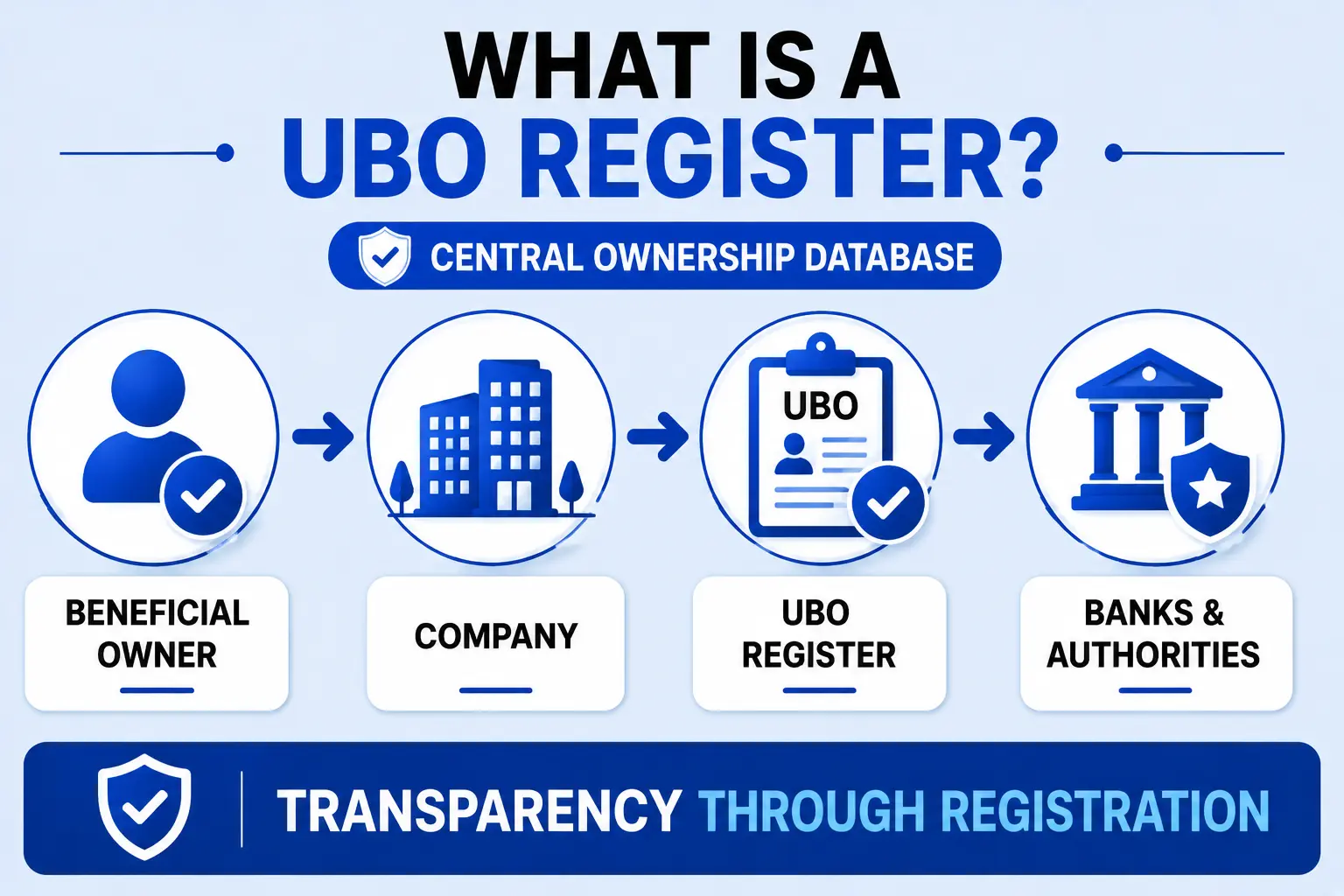

What Is a UBO Register?

A UBO register is a central national database maintained by each EU member state. It records the identity of beneficial owners of companies, trusts, foundations, and other legal arrangements operating under that country’s law.

The legal basis flows through the EU’s 4th AML Directive (2015), 5th AML Directive (2018), and now the 6th AML Directive (2024). Each directive has progressively expanded and tightened the scope of registration obligations. The fragmentation between national implementations – in data fields, access procedures, and timelines – is what 6AMLD is expressly designed to fix.

What Information Is Registered?

| Data Field | Required Under EU Law |

|---|---|

| Full legal name | Yes |

| Month and year of birth | Yes |

| Nationality | Yes |

| Country of residence | Yes |

| Nature of beneficial interest | Yes |

| Extent of beneficial interest (% held) | Yes |

This standardisation is itself a significant 6AMLD reform. Currently, France does not include the UBO’s citizenship in its register, while Spain does not disclose the extent of the beneficial interest. These gaps make cross-border due diligence harder – and 6AMLD mandates a uniform data set across all member states by 2027.

Who Must Register?

The obligation covers limited liability companies, public limited companies, partnerships, foundations, associations, trusts, and any other entity that can hold assets or incur liabilities. In most EU states, the obligation falls on the entity – not the individual UBO – to submit and maintain accurate register entries.

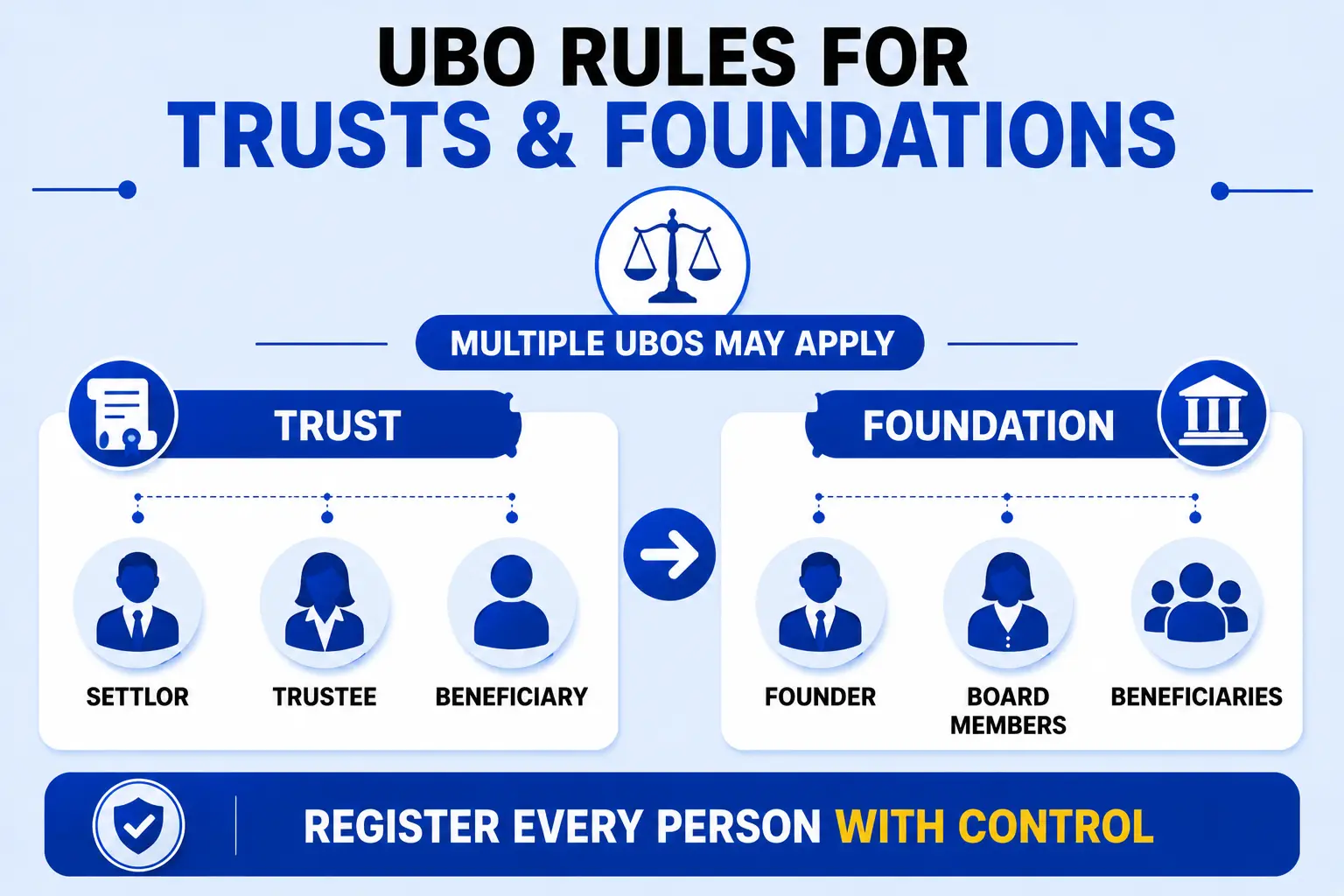

UBO Rules for Trusts and Foundations

While most of the public focus falls on companies, trusts and foundations face their own distinct and often more complex UBO registration obligations. This is an area where compliance errors are particularly common.

Trusts

Express trusts – those created deliberately in writing – must register their beneficial ownership information in the jurisdiction where they are administered. For EU-administered trusts, this typically means registering in the member state where the trustee is resident or where the trust is managed.

The individuals who must be registered as UBOs of a trust are broader than for a company. They include:

- The settlor, the person who created the trust and transferred assets into it

- The trustee(s), the legal owners who manage the trust assets

- The protector, where one is appointed, as they typically hold significant oversight powers

- The beneficiaries, or where the beneficiaries are defined by characteristics rather than named, are the class of persons in whose interest the trust is set up

- Any other person who exercises effective control over the trust

This means a single trust may have four or five separate individuals registered as UBOs in different capacities. Each must be identified, verified, and registered.

Trusts with a connection to EU business – for example, a trust that holds shares in an EU company or that has a trustee resident in an EU member state – fall within the UBO registration framework regardless of where the trust itself was established. A Cayman Islands trust holding shares in an Irish company, administered by a trustee in Dublin, will have UBO registration obligations in Ireland.

Foundations

Foundations are increasingly used in European succession and wealth planning, particularly in jurisdictions such as Austria, Liechtenstein, the Netherlands, and Malta. Their UBO registration obligations mirror those of trusts in most respects – the founder, board members with effective control, and beneficiaries (or the class of beneficiaries) must all be registered.

One important nuance: some EU member states treat private foundations differently from public or charitable foundations. In Belgium, for example, private foundations with no public benefit purpose face the full weight of UBO registration, while certain qualifying charitable foundations may benefit from partial exemptions. Getting specialist advice on which rules apply to a specific foundation structure – and in which jurisdiction – is essential before assuming any exemption applies.

Case Study – Family Foundation and UBO Registration

A Dutch family sets up a private foundation (Stichting) in the Netherlands to hold family assets and manage succession. The foundation owns 100% of a Dutch operating company.

The UBO register in the Netherlands requires registration of the foundation’s beneficial owners. The family members who are the ultimate beneficiaries of the foundation must be registered, along with the foundation’s board members who have effective management control. The operating company, in turn, must register the foundation’s UBOs as its own UBOs – since the foundation is the 100% shareholder, the registration obligation passes through to the underlying company.

Result: two separate UBO registration obligations, at both the foundation and the company level, with the same individuals appearing in both. Both must be updated whenever the beneficiary class or board changes.

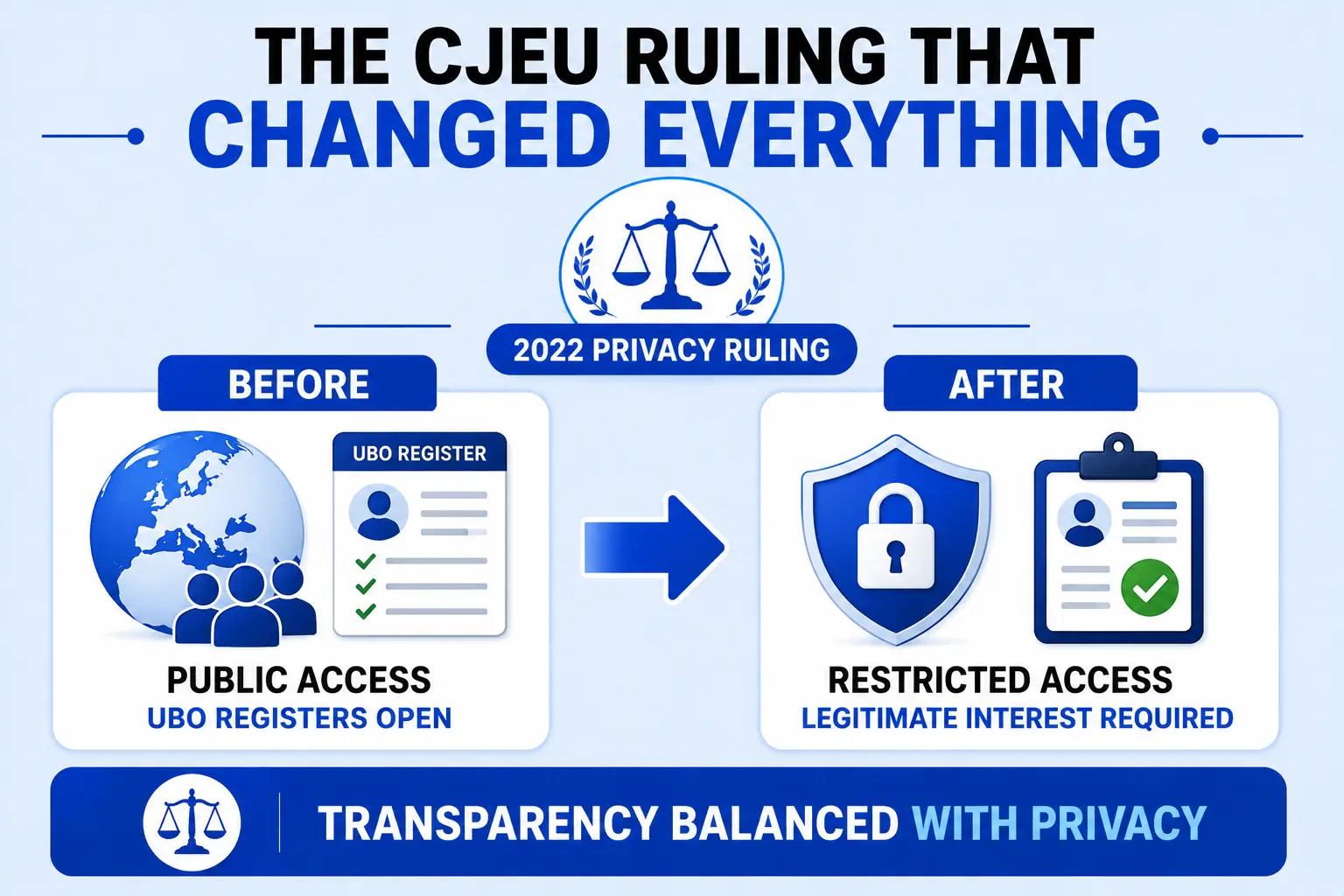

The CJEU Ruling That Changed Everything

In November 2022, the CJEU handed down its judgment in the joined cases WM v Nominee and Sovim SA v Luxembourg Business Registers. The Court struck down the Fifth AML Directive’s provision for unrestricted public access to UBO registers, ruling that it violated the fundamental rights to privacy and data protection guaranteed by the EU Charter.

The impact was immediate. Luxembourg suspended access the same day. Most EU member states closed or restricted their registers within days. The open, searchable register that had been a cornerstone of EU transparency policy since 2018 was effectively dismantled overnight.

Europe moved from open public access to a “legitimate interest” access regime – applicants must actively demonstrate a valid reason for needing UBO data before access is granted.

Who Can Now Access UBO Registers?

- Competent authorities – tax agencies, financial intelligence units, law enforcement, and regulators – retain unconditional access in all member states.

- Obliged entities – banks, payment institutions, lawyers, accountants, notaries, estate agents, and other AML-regulated businesses – can access UBO data for specific customer due diligence purposes, not general searches.

- Journalists, civil society organisations, and academics can access registers upon demonstrating legitimate interest related to AML/CFT investigation or research. Currently, this requires case-by-case applications in most countries, though 6AMLD will introduce presumed legitimate interest for this group.

- Certain third-country entities subject to AML/CFT obligations in their own jurisdiction may access EU registers through bilateral arrangements.

The Fragmentation Problem

Access procedures vary drastically by country – and this is one of the core inefficiencies 6AMLD targets. According to Kyckr’s 2026 analysis, 37% of public access registers can only be accessed using a national ID , effectively blocking foreign entities from accessing data about companies incorporated in those countries (kyckr.com). Some countries use email applications with lengthy processing times. Others use digital portals that require national eID credentials. A bank in Singapore conducting due diligence on an EU-incorporated company may have no reliable path to verify UBO data, despite that data being legally registered.

What 6AMLD Changes in 2026

The EU’s 6th Anti-Money Laundering Directive was enacted in May 2024. Member states must transpose its provisions by 10 July 2026, with full compliance required by 10 July 2027.

According to Transparency International, 48% of EU countries currently offer only limited access, 30% offer public access, and the remainder restrict access to local obliged entities and authorities (transparency.org). 6AMLD is designed to end this fragmentation with hard deadlines and enforceable, binding standards.

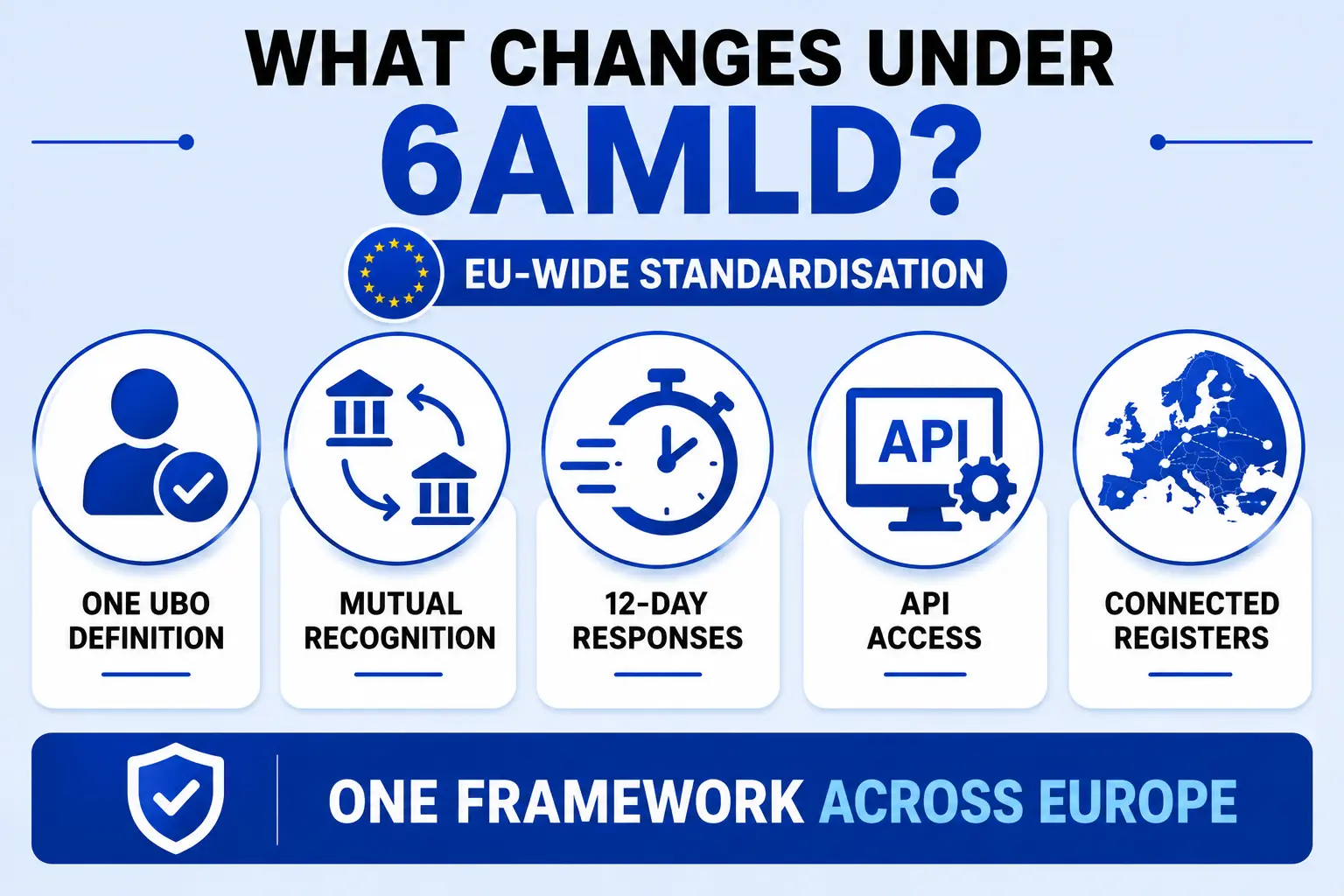

Key Changes Under 6AMLD

- Standardised definition of beneficial owner A single, harmonised definition applies across all EU member states – eliminating country-by-country variation in who qualifies as a UBO.

- Mutual recognition of legitimate interest access Under Article 14, the Commission will create procedures for mutual recognition of legitimate interest access certificates between member states. A certificate issued in Denmark would be recognised when accessing the Dutch or German register, ending the current requirement to apply separately in each country.

- Standardised application templates Article 14 also introduces standardised templates for legitimate interest access requests – ending the situation where each country uses a completely different application format, language, and documentation requirement.

- Presumed legitimate interest for specific groups Journalists, civil society organisations, and academics working on AML-related topics will no longer need to apply on a case-by-case. Legitimate interest is presumed, removing a significant barrier to accountability journalism and civil society monitoring.

- Mandatory response timelines. From 10 November 2026, UBO registers must respond to legitimate interest access requests within 12 working days (extendable to 24 in high-demand periods). Once a 3-year access certificate is issued, repeat requests must be answered within 7 days. Denmark’s register has already aligned with this model – as of January 2026, legitimate interest requests are processed within 12 days, with three-year certificates issued thereafter.

- Machine-readable and API-accessible registers Full digital API access is required by July 2027, enabling automated compliance checks at scale for obliged entities conducting bulk due diligence across multiple jurisdictions.

- Interconnection through BRIS National registers will be linked through the EU Business Register Interconnection System (BRIS), enabling simultaneous cross-border data sharing for competent authorities and obliged entities.

- Lower thresholds for high-risk sectors Member states can apply a 15% threshold in sectors assessed as carrying higher money laundering risk, with EC approval.

6AMLD Timeline at a Glance

| Date | Milestone |

|---|---|

| May 2024 | 6AMLD enacted by EU |

| 10 July 2026 | Member states must transpose key provisions into national law |

| 10 November 2026 | UBO registers must respond to LIA requests within 12 working days |

| 10 July 2027 | Full implementation of all laws, regulations, and technical standards |

Where Transposition Stands in 2026

Progress is uneven. Denmark has already aligned its national law with 6AMLD requirements. Sweden issued detailed legal guidance in December 2025 on how it will handle legitimate interest access – three-year certificates, EU mutual recognition, and restrictions on non-EEA applicants. By contrast, Czechia fully closed its public beneficial ownership register in December 2025 pending implementation of the new legitimate interest framework – a reminder that register access can disappear entirely during the transition period. Companies that relied on public access for due diligence purposes in Czechia had to pivot to alternative verification methods overnight.

Country-by-Country Overview: Key UBO Registers in Europe

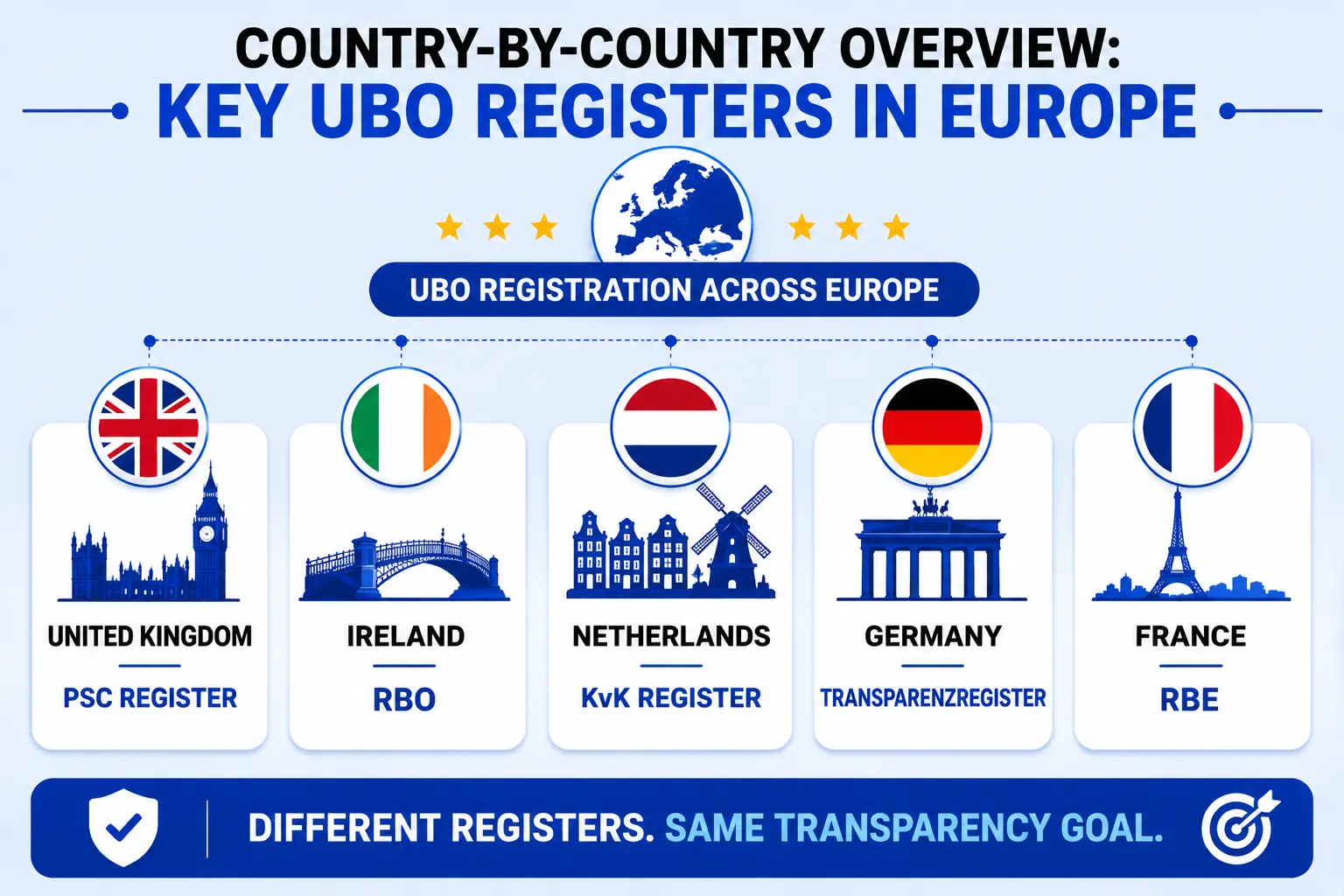

United Kingdom – PSC Register

The UK’s Persons with Significant Control (PSC) Register at Companies House is the most transparent beneficial ownership register in Europe.

- Threshold: 25%

- Access: Fully public and API-accessible – no legitimate interest required

- Update deadline: Within 14 days of any change

- 2026 update: Identity verification requirements for directors and PSCs under the Economic Crime and Corporate Transparency Act 2023. Companies House now has powers to query and reject suspicious filings.

- Penalties: Unlimited fines and up to 2 years’ imprisonment for false statements

The UK operates outside the EU legal framework post-Brexit, but its PSC obligations run parallel to – and in several respects exceed – EU UBO requirements.

Ireland – RBO (Register of Beneficial Ownership)

- Threshold: 25%

- Access: Legitimate interest only (post-CJEU)

- Registration deadline: Within 5 months of incorporation

- Annual confirmation: Required regardless of whether any changes have occurred

- Key banking requirement: Banks require RBO confirmation before opening corporate accounts – making RBO compliance a practical prerequisite for doing business in Ireland

- Penalties: Up to €500,000 for non-compliance; directors can be held personally liable

Netherlands – KvK UBO Register

- Threshold: 25%

- Access: Legitimate interest only

- Registration deadline: Within 10 days of incorporation – one of the tightest deadlines in Europe

- Update deadline: Within 7 days of any change, also among the strictest

- Penalties: Criminal prosecution possible for deliberate non-disclosure

Germany – Transparenzregister

- Threshold: 25%

- Access: Legitimate interest only

- Key rule: All companies must file directly. The “cascade rule” – which previously allowed automatic derivation from the commercial register – was removed in 2021. Every entity must make an active, explicit filing.

- Penalties: Up to €1,000,000 for serious non-compliance – the highest civil penalty in the EU for UBO violations

France – RBE (Registre des Bénéficiaires Effectifs)

- Threshold: 25%

- Access: Legitimate interest only; held at the Greffe du Tribunal de Commerce

- Update deadline: Within 30 days of any change

- Notable gap: France currently excludes UBO citizenship from its register – a gap 6AMLD’s standardised data set will close

- Penalties: Up to €7,500 for individuals; higher for deliberate or repeated non-compliance

Belgium

- Threshold: 25%

- Access: Legitimate interest only

- Annual confirmation: Required every year, even if nothing has changed

- Update deadline: Within 30 days of any change

- Consequences: Non-compliant companies can be struck from the Crossroads Bank for Enterprises, making them unable to operate legally in Belgium

Estonia – e-Business Register

Estonia’s beneficial ownership register remains one of the most digitally advanced and publicly accessible in Europe.

- Threshold: 25%

- Access: Publicly accessible

- Update process: Fully digital and integrated with Estonia’s national digital identity system

Italy

- Threshold: 25%

- A March 2026 decree introduces Articles 21-bis through 21-septies, creating new access categories and protection mechanisms for UBOs who can demonstrate a disproportionate personal security risk from disclosure

- Full 6AMLD transposition deadline: July 2027

Spain – Registro Mercantil

- Threshold: 25%

- Registry: Held within the Mercantile Registry

- Access procedures are evolving under 6AMLD transposition; full implementation expected by July 2027

Nominee Directors, Nominee Shareholders, and UBO Rules

This is one of the most misunderstood areas in corporate compliance. The critical point: using a nominee does not remove your UBO obligation.

What Nominee Arrangements Actually Mean

When a nominee director or nominee shareholder is appointed, two sets of identities become relevant:

- The nominee appears in the commercial register (as director or shareholder on record)

- The beneficial owner – the person who gives instructions to the nominee and enjoys the economic benefit – must be disclosed in the UBO register

Both are identifiable. The nominee is visible in public company records. The UBO is visible in the beneficial ownership register to those with legitimate access. These are complementary forms of disclosure, not alternatives.

Legitimate Reasons to Use Nominee Arrangements

Nominee services remain entirely lawful and commercially useful. Common legitimate purposes include:

- Operational privacy from the general public (the UBO register, post-CJEU, is not open to all – it is restricted to those with legitimate access)

- Administrative convenience in foreign jurisdictions where the beneficial owner is not locally present

- Corporate flexibility in multi-entity group structures

Tax transparency and AML obligations still apply in full, however, regardless of any nominee arrangement.

Documentation Requirements

A formal legal instrument must underpin every nominee arrangement. For nominee shareholders, this is typically a Declaration of Trust. For nominee directors, a Service Agreement defines the relationship. These documents:

- Confirm that the nominee acts solely on the beneficial owner’s instructions

- Establish the legal relationship between nominee and UBO for regulatory and banking purposes

- Are required by most banks as part of corporate account opening due diligence

- Must be available for production to regulators or competent authorities on request

Regulators increasingly treat undocumented nominee arrangements as red flags. The absence of a Declaration of Trust, for example, raises questions about whether the nominee arrangement is a legitimate commercial tool or an attempt to conceal ownership. Proper documentation protects both the nominee service provider and the beneficial owner.

Real-World Example – Ireland Nominee Structure

A Swiss-based entrepreneur incorporates a holding company in Ireland. He appoints a nominee director and a nominee shareholder through UCI. Under Irish RBO rules, he must register as the UBO within 5 months of incorporation. His bank in Dublin requests RBO confirmation before opening the company account. The nominee director’s name appears in the Companies Registration Office records. The entrepreneur’s name sits in the RBO – accessible to banks and competent authorities. His Declaration of Trust documents the full arrangement.

Result: full legal compliance, operational privacy preserved from the general public, and banking access secured. The nominee arrangement works exactly as intended – but only because the UBO registration obligation has been met.

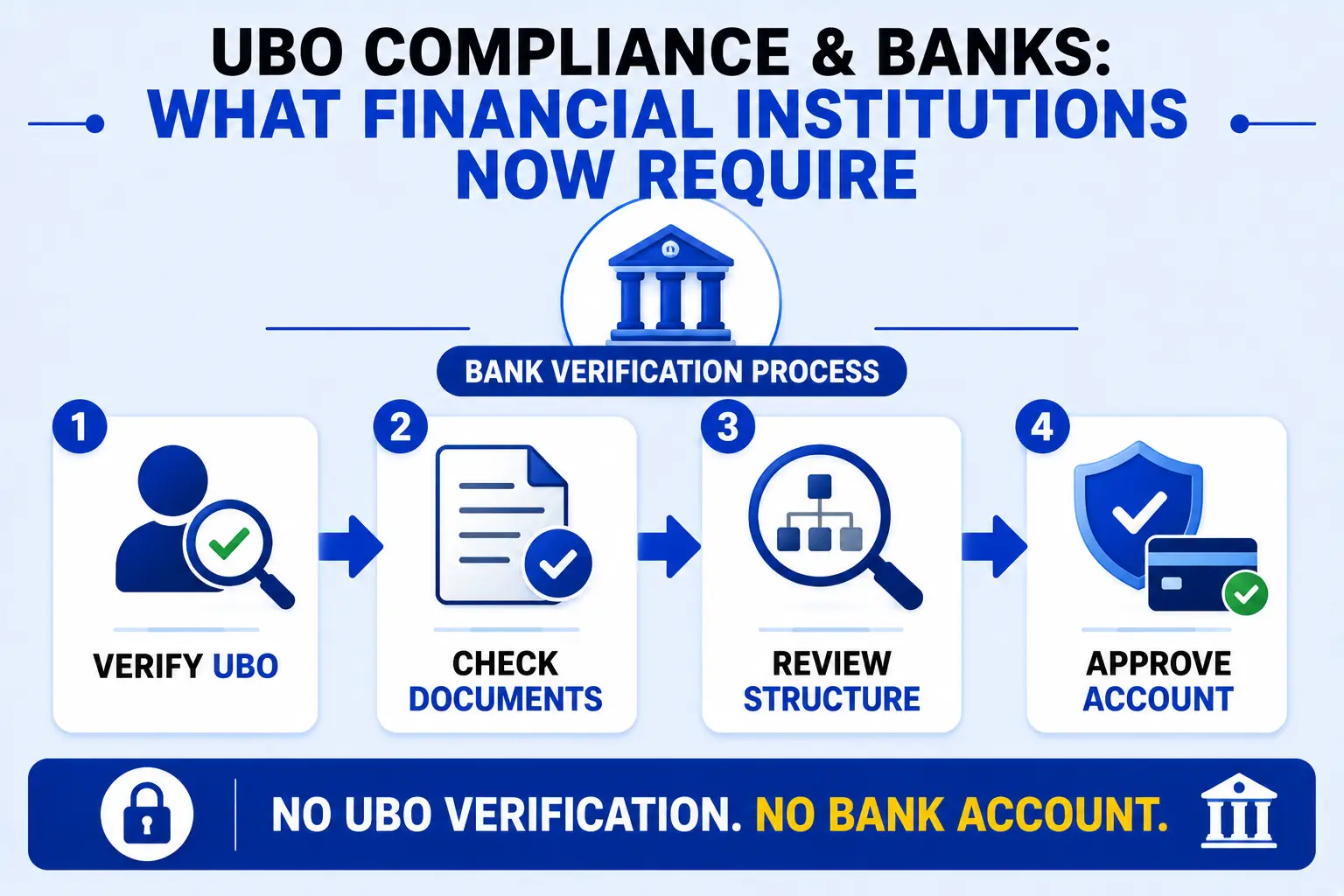

UBO Compliance and Banks: What Financial Institutions Now Require

Banks across Europe have significantly tightened their UBO verification requirements since 2022, and especially since the introduction of the EU AML Regulation in 2024.

What Banks Check During Corporate Account Opening

When a company applies to open a corporate bank account in an EU country, the bank must conduct full customer due diligence (CDD), which includes verifying the beneficial ownership of the entity. Banks will typically require:

- UBO register confirmation: A certificate or official extract from the national UBO register confirming the entity’s registered beneficial owners

- Passports or national ID for each UBO: Identity verification for every individual above the 25% threshold

- Explanation of ownership structure: For multi-layer or international structures, a written description of the ownership chain

- Declaration of Trust (where nominees are used): Formal documentation of nominee arrangements must be available on request

Banks in Ireland have made this explicit – RBO registration is a hard prerequisite for account opening. Dutch, German, and Belgian banks follow similar requirements.

Enhanced Due Diligence for Complex Structures

If a company’s ownership involves nominee arrangements, international holding structures, or beneficial owners in jurisdictions assessed as higher risk, banks will apply enhanced due diligence (EDD) . This involves deeper source-of-funds verification, additional documentation, and increasingly automated UBO data checks against national registers and third-party data providers.

Financial institutions with UBO verification requirements must ensure they have the necessary processes and tools in place to correctly identify and verify the UBOs of their customers, since it is only possible to properly risk-score a customer and carry out the right level of customer due diligence if UBOs are fully known.

Use Case – Multi-Jurisdiction Structure

A German GmbH is 100% owned by a Maltese holding company. The Maltese company is 80% owned by a Luxembourg SARL, which is in turn 100% owned by an individual in the UAE.

The German bank opening an account for the GmbH must trace the ownership chain through Malta and Luxembourg to the UAE individual, who is the UBO at 80% indirect ownership. The bank requires: the UBO’s passport, the Luxembourg SARL’s UBO registration, the Maltese company’s beneficial ownership declaration, and an explanation of the group structure.

Without all of this, the account opening is refused. This is now standard practice – not an exception.

AMLA: The New EU-Wide AML Supervisor

One of the most significant structural changes in the 2024 EU AML package is the creation of the Anti-Money Laundering Authority (AMLA) – a new EU-level supervisory body headquartered in Frankfurt. AMLA represents a step-change in how AML compliance is enforced across the EU, and it has direct implications for UBO compliance.

What AMLA Does

AMLA’s mandate covers two levels of supervision. For a defined group of high-risk financial institutions operating across multiple EU member states, AMLA will exercise direct supervision – meaning it will conduct its own inspections, request information, and impose sanctions without going through national authorities. For the wider population of obliged entities, AMLA will provide indirect supervision, coordinating and overseeing national supervisors to ensure they apply AML rules consistently.

For UBO compliance specifically, AMLA’s role is significant in three ways:

- Cross-border enforcement coordination. Previously, a company that was non-compliant with UBO rules in Germany but had no other EU presence could largely avoid consequences beyond German borders. Under AMLA’s coordination role, a non-compliance finding in one member state can trigger coordinated action across all EU jurisdictions where the same group operates.

- Supervisory convergence. AMLA is tasked with producing binding technical standards, guidelines, and supervisory methodologies that national authorities must follow. This means the standard for what counts as adequate UBO verification – by both companies and obliged entities – will be set at EU level, not left to national discretion.

- Information sharing. AMLA operates a central information database linking national AML supervisors, FIUs, and UBO registers. This infrastructure makes it materially easier for any one authority to identify patterns of non-compliance that might not be visible from a single national perspective.

Timeline for AMLA Supervision

AMLA formally began operations in 2025. Direct supervision of selected high-risk entities begins in 2027, following a selection process currently underway. National supervisors are expected to align their methodologies with AMLA technical standards from 2026 onwards – meaning the practical effect of AMLA’s existence will be felt before direct supervision formally begins.

For companies with multi-country EU operations, the message is clear: AMLA makes consistent, group-wide UBO compliance more important – not just compliance in each jurisdiction taken in isolation.

What Happens If You Don’t Comply?

Non-compliance with UBO registration obligations is treated seriously across the EU, with financial, operational, and reputational consequences.

Penalties Across Key Jurisdictions

| Country | Maximum Penalty | Criminal Sanctions? |

|---|---|---|

| Germany | €1,000,000 (civil) | No |

| UK | Unlimited fines + 2 years imprisonment | Yes |

| Ireland | €500,000 | No (directors liable personally) |

| Italy | Variable | Yes – for false declarations |

| Netherlands | Prosecution possible | Yes – for deliberate non-disclosure |

| Belgium | Fines + CBE removal | No |

| France | €7,500 (individuals) | No |

Beyond Financial Penalties

- Banks will refuse to open or maintain accounts for entities with incomplete UBO registration. In some cases, existing accounts have been suspended where banks cannot verify UBO information on request.

- Professional advisers face their own sanctions. Lawyers, accountants, and corporate service providers who assist in structuring non-compliant arrangements face regulatory penalties, including suspension from practice and personal fines.

- Reputational damage can be long-lasting. UBO breaches are increasingly treated as governance failures rather than administrative oversights. Investors, counterparties, and institutional partners conduct their own UBO checks and may exit relationships where compliance gaps are identified.

- AMLA escalation. As AMLA begins cross-border supervisory work, a UBO non-compliance issue in one jurisdiction may trigger a review of a company’s entire European footprint – not just the country where the breach occurred.

Practical Compliance Checklist for 2026

Use this checklist to assess your current position before the July 2026 deadline.

- Step 1 – Map your full ownership chain. Identify every entity in your corporate group and trace ownership to the ultimate natural persons. Apply the 25% threshold at each level. Document every indirect holding calculation.

- Step 2 – Identify all UBOs. For each entity, identify every individual who meets the 25% threshold (directly or indirectly) or exercises control through other means. Where no individual meets the threshold, identify the senior managing official.

- Step 3 – Register in every relevant jurisdiction. File UBO information with the register in each EU country where you have a legal entity. Confirm deadlines: Ireland (5 months), Netherlands (10 days), UK (14 days), France and Belgium (30 days).

- Step 4 – Document all nominee arrangements. Ensure every nominee director and shareholder arrangement is supported by a signed Declaration of Trust or equivalent instrument. Verify documentation is current and available for production to banks and regulators.

- Step 5 – Build a change-management process. Assign internal responsibility for monitoring ownership changes. When a UBO changes – through share transfer, restructuring, or death – trigger a register update within the applicable deadline.

- Step 6 – Confirm annual obligations. Ireland and Belgium require annual confirmations even when nothing has changed. Diarise these obligations with adequate lead time.

- Step 7 – Understand your access exposure. Determine who currently has legitimate access to your UBO information in each jurisdiction, and how 6AMLD changes will affect that, particularly the expanded presumed legitimate interest for journalists and civil society.

- Step 8 – Assess any exemptions. Certain listed companies on regulated markets and some government-owned entities qualify for partial exemptions. Some foundations may also be partially exempt depending on the jurisdiction.

- Step 9 – Track 6AMLD transposition in your key jurisdictions. Monitor national implementation progress. Denmark and Sweden are ahead; Czechia temporarily suspended register access during transition. Know where your key jurisdictions stand.

- Step 10 – Prepare for AMLA oversight. Review whether any entities in your group fall within AMLA’s direct supervisory scope. If so, prepare for a materially higher level of scrutiny from 2027 onwards.

Conclusion

The era of opaque ownership structures in Europe is over. The 2022 CJEU ruling, the 6AMLD transparency framework, and AMLA’s cross-border supervisory mandate are collectively raising the bar for beneficial ownership compliance to a level not seen before. The fragmentation that previously allowed companies to exploit gaps between national regimes is closing – fast.

The practical message is clear. Nominee arrangements remain fully legal and commercially valuable – but they must be properly documented, and UBO registration obligations must be met in full in every jurisdiction where you hold a legal entity. Incomplete filings, outdated register entries, and undocumented nominee structures are no longer low-risk oversights. They are active compliance exposures with real financial, operational, and reputational consequences.

The July 2026 deadline is not a distant milestone. For companies with multi-jurisdictional structures, complex ownership chains, or nominee arrangements, the compliance work needs to start now – before transposition deadlines arrive and before AMLA has the tools to act across borders.