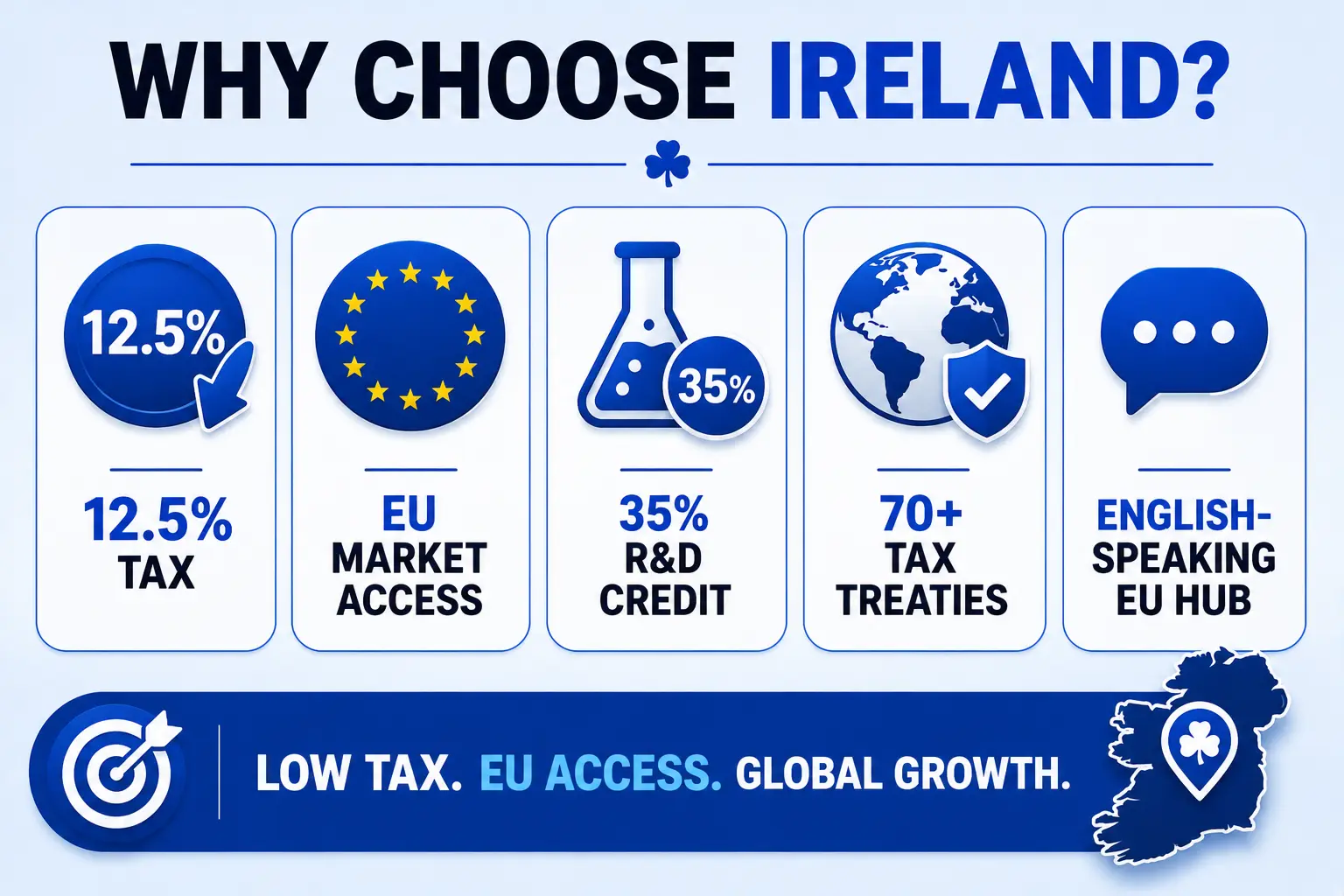

Ireland has established itself as one of the most attractive destinations for international business in Europe. It is the only English speaking EU member state, it offers a 12.5% corporate tax rate on trading income, and it provides full access to the EU single market. For UK businesses that lost their EU passporting rights after Brexit, Ireland has become the default gateway back into Europe. For US and non EU technology companies, Ireland is the obvious choice: Google, Meta, Apple, LinkedIn, and Salesforce all anchor their European headquarters here.

2026 is a particularly relevant year to consider Irish company formation. Ireland’s Auto Enrolment pension scheme came into effect in January 2026, creating new payroll obligations for employers. The OECD Pillar Two global minimum tax now applies to large multinational groups operating in Ireland. And Ireland’s R&D tax credit has been increased to 35% of qualifying expenditure, strengthening an already competitive innovation incentive landscape.

This guide covers everything you need to set up a company in Ireland in 2026. We explain the right legal structure for your situation, walk through each step of the Companies Registration Office process, clarify the director and residency rules that trip up many non-resident founders, break down the Irish tax regime, and set out the ongoing compliance calendar you need to manage once your company is live. We also give you a realistic picture of costs and the most common mistakes to avoid.

UCI Ltd can handle every step of your Irish company formation, from initial name check through to your Certificate of Incorporation and tax registration.

Why Set Up a Company in Ireland?

Ireland consistently attracts more foreign direct investment per capita than almost any other EU member state. Understanding why helps you assess whether Irish company formation is the right move for your specific business goals.

The 12.5% Corporate Tax Rate

Ireland’s headline corporate tax rate of 12.5% applies to all active trading income. This rate has been in place since 2003 and successive Irish governments have repeatedly committed to maintaining it as a cornerstone of national economic policy. For international comparison, the EU average corporate tax rate sits at approximately 21%, and the UK rate is 25%. The stability of the Irish rate matters as much as its level: businesses can plan long-term with confidence.

It is important to note that the 12.5% rate applies to trading income. Passive income, including investment returns, rental income, and income from financial assets, is taxed at 25%. Companies need to ensure that their Irish entity conducts genuine trading activity to access the lower rate.

For large multinational groups with global consolidated revenues above 750 million euros, the OECD Pillar Two rules now require a minimum effective tax rate of 15%. Ireland has implemented these rules in domestic legislation. For the vast majority of small and medium sized businesses, Pillar Two does not apply.

Full Access to the EU Single Market

An Irish registered company is an EU company. This means it can sell goods and services across all 27 EU member states under single market rules, without import duties, regulatory barriers, or the need for local subsidiaries in each country. For UK businesses that lost EU market access after Brexit, this is the single most important practical reason to incorporate in Ireland.

Ireland is also the only English speaking EU country remaining after Brexit. This makes it the obvious base for US, Canadian, Australian, and UK founded businesses that want an EU presence but do not want to operate in a second language or navigate an unfamiliar legal system.

The R&D Tax Credit

Ireland’s Research and Development tax credit has been increased to 35% of qualifying R&D expenditure from 2026, up from the previous 25% rate. This is one of the most generous R&D incentives in Europe. The credit applies to systematic investigation, scientific or technological research, and experimental development activities. Importantly, companies can receive the credit as a cash payment from Revenue even if they have no corporation tax liability, making it directly valuable to early stage and loss making companies. Source: corpenza.com.

The Knowledge Development Box

Ireland’s Knowledge Development Box (KDB) applies an effective tax rate of 6.25% to profits derived from qualifying intellectual property. Qualifying assets include patents, copyrighted software, and certain computer programs that result from R&D activity. The KDB makes Ireland particularly attractive for technology companies, pharmaceutical businesses, and any organisation that monetises IP at scale.

Strong Talent Pool and Business Ecosystem

Ireland’s investment in third-level education has produced a highly skilled graduate workforce. The country has one of the youngest and most educated populations in the EU. Major technology, pharmaceutical, financial services, and professional services clusters have developed around Dublin, Cork, Galway, and Limerick. This means companies incorporated in Ireland have genuine access to talent, not just a tax address.

The Irish government’s IDA (Industrial Development Authority) actively supports foreign direct investment with grants, supports, and advisory services for qualifying businesses.

Common Law Legal System

Ireland operates under a common law legal system that shares its foundations with UK and US commercial law. Contract structures, corporate governance frameworks, employment law concepts, and intellectual property protections are all familiar to English-speaking international founders and their legal advisors. This reduces legal advisory costs and speeds up commercial transactions.

Double Tax Treaties

Ireland has an extensive network of double taxation agreements with over 70 countries, including the United States, the United Kingdom, Germany, France, China, and Japan. These treaties prevent companies from being taxed twice on the same income and are essential for groups with cross-border royalty flows, dividend payments, or management fee structures.

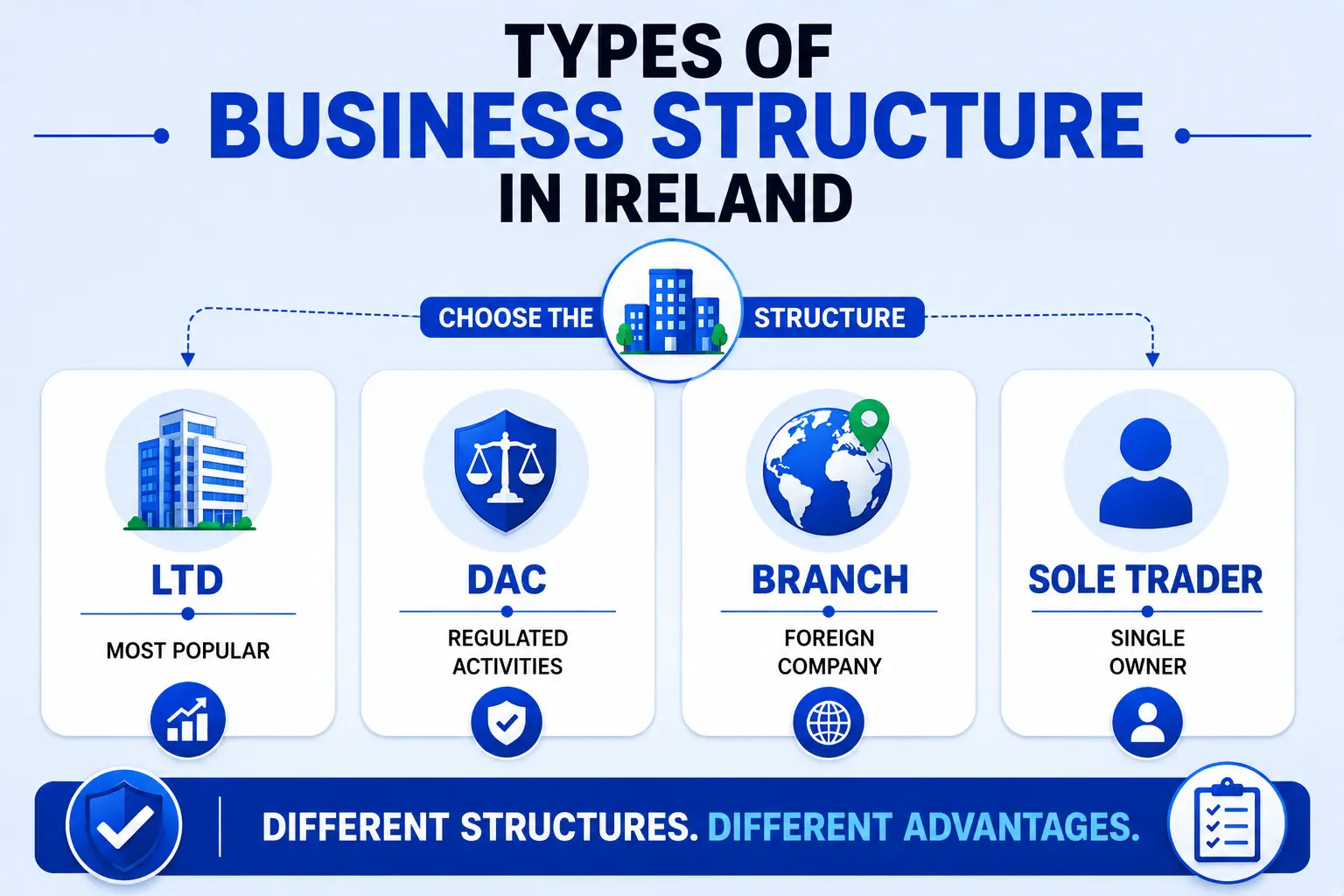

Types of Business Structure in Ireland

Selecting the right legal structure is the foundation of your Irish company formation. The choice affects your tax position, liability exposure, governance requirements, and how investors and customers perceive your business.

Private Company Limited by Shares (LTD)

The LTD is by far the most common structure chosen by both domestic and international founders. It is the default choice for startups, consultancies, technology companies, e-commerce businesses, and professional service firms. Here is why it dominates:

- It is a separate legal entity, meaning the company’s debts and obligations belong to the company, not to its directors or shareholders personally.

- Shareholders’ liability is limited to the amount they have paid (or agreed to pay) for their shares. If a shareholder holds one share worth one euro, their maximum liability in a winding up is one euro.

- Only one director is required, making it suitable for sole founders.

- There is no minimum share capital requirement. Most companies are incorporated with a nominal share capital of 100 euros.

- The company can issue different classes of shares, making it straightforward to bring in investors, create employee share option plans, or structure founder equity.

- It benefits from the full range of Irish tax reliefs, including the 12.5% trading rate, R&D tax credit, and the Knowledge Development Box.

Designated Activity Company (DAC)

The DAC is a company with a defined and restricted set of objects. Its constitution must specify the activities the company is permitted to carry on, and the company cannot legally act outside those objects. The DAC is most commonly used in regulated sectors such as financial services, fund administration, and structured finance. It requires at least two directors. For most international founders setting up a trading business, the LTD is more appropriate than the DAC.

Public Limited Company (PLC)

A PLC can offer its shares to the public and is the structure required for companies seeking a listing on a stock exchange. It requires a minimum allotted share capital of 25,000 euros, at least 25% of which must be paid up before the company can commence business. PLCs are subject to significantly more regulatory scrutiny than LTDs. Unless you are specifically planning a public fundraise or stock market listing, a PLC is not the right structure at incorporation.

Branch of a Foreign Company

A foreign company can register a branch in Ireland under the Companies Act 2014 without creating a new legal entity. The branch is an extension of the parent company rather than a standalone corporate structure. This means the parent company bears full legal and financial responsibility for the branch’s activities. Branches must file accounts with the CRO but are generally subject to lighter governance requirements than incorporated companies. A branch may be appropriate for a company that wants to test the Irish market before committing to full incorporation, or where group structure considerations make a new entity undesirable.

Sole Trader and Partnership

Sole traders and partnerships are simpler to establish but carry unlimited personal liability. The individual or partners are personally responsible for all debts and obligations of the business. For any business with meaningful commercial exposure, employee relationships, contracts, or external investment, a limited liability structure is strongly preferable. Non Irish residents who operate as sole traders in Ireland may also face significant tax complications.

Comparison of the three most relevant structures for international founders:

| Feature | LTD | DAC | Branch |

| Separate legal entity | Yes | Yes | No (parent is liable) |

| Minimum directors | 1 | 2 | 1 |

| Minimum share capital | None | None | Not applicable |

| Liability protection | Yes | Yes | No |

| Objects clause required | No | Yes | No |

| Best suited to | Startups, SMEs, tech, services | Regulated sectors, finance | Market testing, group structures |

| CRO registration required | Yes (Form A1) | Yes (Form A1) | Yes (Form F12) |

| Audit exemption available | Yes (small companies) | Yes (small companies) | Depends on parent |

Key Requirements Before You Incorporate

Before you can file with the Companies Registration Office, you need to have certain elements confirmed and ready. Getting these right before you start the filing process saves time and avoids resubmissions.

Company Name

Your company name must be unique and distinguishable from all names already registered on the CRO register. You can check availability using the CORE portal at core.cro.ie. The name check is free and instant. Once you have confirmed availability, you can reserve the name for 28 days while you prepare the remaining incorporation documents.

Certain words are restricted and require prior approval from the relevant regulator before they can be included in a company name. These include words such as bank, insurance, assurance, building society, credit union, university, and national. If your proposed name includes any regulated term, factor in additional time for the approval process.

The name must end with Limited or Ltd (or the Irish language equivalents Teoranta or Teo) for an LTD. The name should not be misleading as to the nature of the business.

Registered Office Address

Every Irish registered company must maintain a registered office address in Ireland. This is the address to which all official correspondence, regulatory notices, and legal documents will be sent. It must be a physical address in Ireland. A PO box does not qualify. A virtual office address provided by a company formation agent or business centre is acceptable and is the most common solution for non resident founders.

The registered office address is publicly listed on the CRO register. It does not need to be the company’s principal place of business or where its employees are based. Annual costs for a virtual registered office address in Dublin typically range from 200 to 500 euros per year.

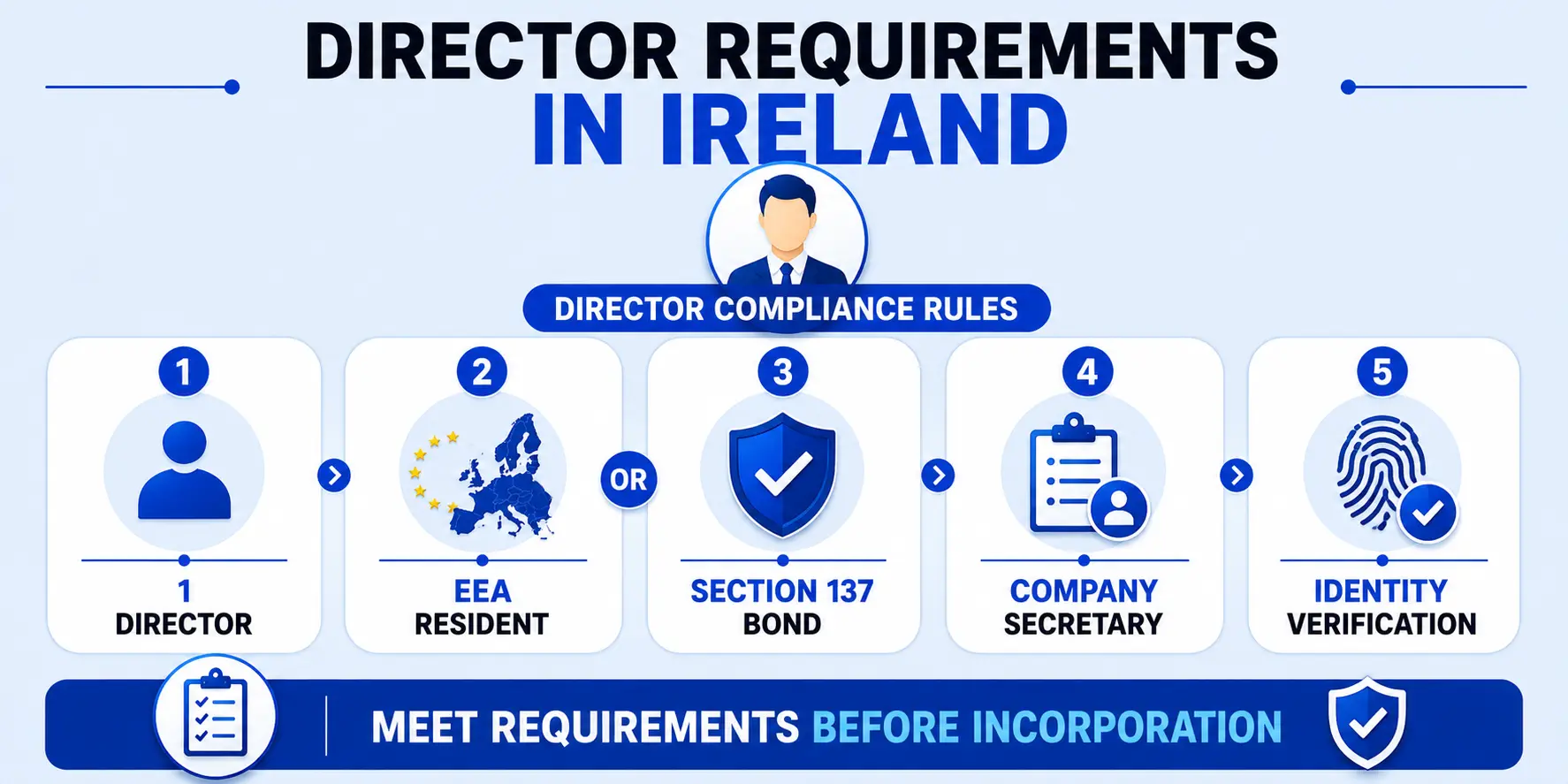

Directors and the EEA Residency Requirement

An Irish LTD requires at least one director. However, under Section 137 of the Companies Act 2014, at least one director must be ordinarily resident in a European Economic Area member state. The EEA comprises the 27 EU member states plus Norway, Iceland, and Liechtenstein.

Since the UK left the EU on 31 January 2020, UK residents no longer qualify as EEA residents. This is one of the most common points of confusion for UK-founded businesses seeking to incorporate in Ireland. A UK resident director can still serve on the board of an Irish company, but their presence does not satisfy the Section 137 EEA residency requirement.

If no EEA resident director is appointed, the company must obtain a Section 137 non-resident director bond before the CRO will accept the incorporation application. This bond is an insurance-backed guarantee that the company will comply with its obligations under Irish company and tax law. The bond typically costs between 1,500 and 2,000 euros for two years and is arranged through authorised insurers or formation agents.

An alternative to the bond is to appoint a professional nominee EEA resident director. Several Irish company formation agents and corporate service providers offer this service for an annual fee. The nominee director has no involvement in the day-to-day running of the business but satisfies the legal requirement.

Company Secretary

Every Irish company must have a company secretary. The company secretary is responsible for maintaining the company’s statutory records, filing documents with the CRO and Revenue on time, and ensuring the company complies with its ongoing obligations under the Companies Act 2014. If the company has only one director, the secretary must be a different person or entity. Corporate secretarial services are widely available from formation agents and accounting firms.

Share Capital and Constitution

There is no minimum share capital requirement for an Irish LTD. The vast majority of companies are incorporated with a nominal share capital of 100 euros, typically comprising 100 shares with a par value of one euro each. The initial share capital does not need to be paid in full at the time of incorporation.

The Constitution is the company’s governing document. An LTD is a single document that combines the memorandum and articles of association. The CRO provides a model constitution suitable for straightforward single-founder or small-shareholder structures. If your company involves multiple co-founders, different share classes, investor protections, preemption rights, drag-along and tag-along provisions, or employee share option plans, you should have a bespoke constitution drafted by a solicitor.

Personal Public Service Numbers and Identity Verification

All directors, secretaries, and beneficial owners must complete identity and address verification in compliance with anti-money laundering requirements. Each director must submit a Form VIF (Verification of Identity Form) with their incorporation application. For non-Irish residents who do not have a Personal Public Service (PPS) Number, an Individual Person Number (IPN) can be obtained from the CRO for the purpose of company registration. If a beneficial owner does not have a PPS Number, a BEN2 form is required for RBO registration.

Step by Step: How to Register a Company in Ireland (CRO)

The CRO registration process is straightforward when you know what is required at each stage. Here is a complete walkthrough from name check to operational company.

Step 1: Choose Your Company Type and Name

Decide on the appropriate legal structure for your business. For the overwhelming majority of non resident founders, an LTD is the right choice. Once you have settled on the structure, check name availability on the CORE portal at core.cro.ie and reserve your preferred name. The reservation lasts 28 days and gives you time to prepare documents without the risk of another company taking the name.

Think ahead about your brand identity. If you intend to trade under a business name that differs from your company name (for example, your company is registered as Smith Technology Limited but you trade as CloudPath), you will also need to register the business name separately with the CRO under the Registration of Business Names Act 1963.

Step 2: Prepare Incorporation Documents

The core documents required are:

- Form A1: The main incorporation form. It captures the company name, registered office address, details of all directors and the company secretary (including their names, addresses, dates of birth, and occupations), shareholder information and share distribution, a description of the company’s business activity, and confirmation that the Section 137 EEA residency requirement is satisfied or that a bond is in place.

- Company Constitution: The governing document, signed by all founding members. Either the CRO model constitution or a bespoke version prepared by a solicitor.

- Form VIF: Identity verification for each director. Requires certified copies of a passport or national identity card plus proof of current address.

- Section 137 Bond (if required): Confirmation from the bonding insurer or a statutory declaration confirming EEA residency.

Formation agents such as UCI Ltd will prepare all of these documents on your behalf, collect the required signatures remotely, and manage the filing process.

Step 3: Submit to the CRO via the CORE Portal

All documents are submitted through the CRO’s CORE online portal at core.cro.ie. The standard CRO registration fee is 50 euros for electronic applications. A reduced fee of 25 euros applies where an online-only model constitution is used.

Standard processing time is 10 working days from receipt of a complete and valid application. Expedited processing (for an additional fee) reduces this to 5 working days. All documents must be correctly completed and signed before submission: incomplete or inconsistent applications are returned for correction, which resets the processing clock.

Step 4: Receive Your Certificate of Incorporation

Once the CRO is satisfied with the application, it issues a Certificate of Incorporation. This certificate is the legal proof that your company exists as a separate legal entity under Irish law. It includes your Company Registration Number (CRN), which you will use for all dealings with the CRO and Revenue going forward. From the date on the certificate, your company can legally enter into contracts, open bank accounts, and conduct business.

Step 5: Register for Tax with Revenue Commissioners

CRO registration and tax registration are separate processes. Incorporation does not automatically register your company with Revenue. You must file a TR2 form through the Revenue Online Service (ROS) at ros.ie. The TR2 covers:

- Corporation Tax: Mandatory registration. Must be completed within 30 days of commencing activity. Revenue will then issue your company’s tax reference number.

- VAT: Registration is mandatory once annual turnover exceeds 42,500 euros for services or 85,000 euros for goods. Voluntary registration before reaching these thresholds is possible and often advantageous, particularly for businesses that incur significant VAT on their purchases.

- PAYE, PRSI, and USC: Registration is required once the company pays any salary or wages in Ireland, including to a director.

Tax registration typically takes 2 to 5 working days from submission of the TR2 form.

Step 6: Register Beneficial Owners with the RBO

The Central Register of Beneficial Ownership (RBO) is a public register maintained by the CRO. Any individual who ultimately owns or controls 25% or more of the company’s shares or voting rights must be registered. Registration must be completed within 5 months of incorporation.

In practice, most Irish banks will not proceed with opening a business bank account until the company can confirm its RBO registration is complete. Do not delay this step. If a beneficial owner does not have an Irish PPS Number, a BEN2 form must be submitted to the RBO along with supporting identity documents.

Step 7: Open a Business Bank Account

Opening a business bank account is the final practical step before your company is fully operational. You have two main options in Ireland:

- Traditional Irish banks (AIB, Bank of Ireland, Ulster Bank): Comprehensive business banking services including credit facilities, merchant services, and business advisory support. The application and due diligence process typically takes 2 to 6 weeks. Many traditional banks require at least one director to attend an in person meeting, which can be a logistical challenge for non-resident founders.

- Digital banking and EMI alternatives (Revolut Business, Wise Business, Stripe): Fully online application process, typically completed within 24 to 72 hours. Suitable for companies that primarily operate online or internationally. Note that digital banking providers do not offer lending facilities or the same range of services as traditional banks.

Documents required for bank account opening include: Certificate of Incorporation, Company Constitution, director identification and proof of address, RBO confirmation, and a short description of the business’s activities and expected transactions.

Real World Example: How a UK Founder Set Up an Irish Company Post Brexit

Case Study: London-Based B2B SaaS Startup

Background

A London-based founder had built a B2B software platform with 12 paying customers, eight of whom were based in continental Europe. After Brexit, several EU customers raised concerns about contracting with a UK entity for data processing and compliance reasons. The founder needed an EU-registered company to continue growing the European customer base.

Structure and Setup

The founder incorporated an Irish LTD through a formation agent. As neither the founder nor the co-founder was EEA resident, a Section 137 non-resident director bond was obtained for 1,750 euros for a two-year period. A virtual registered office address in Dublin was arranged at 400 euros per year. A nominee EEA resident director was also appointed through the formation agent.

Timeline

The Certificate of Incorporation was received within 7 working days of the complete application being submitted. Corporation Tax and VAT registration was completed within 4 days of filing the TR2 form. A Revolut Business account was opened within 48 hours. Total time from starting the process to having an operational Irish company with a bank account: 13 working days.

Outcome

All eight EU customers were successfully migrated to contracts with the new Irish entity within 30 days of incorporation. The Irish company subsequently benefited from the 12.5% corporation tax rate on its European trading profits and filed a successful R&D tax credit claim in its first full year of operation.

Director Requirements in Detail

The director rules are one of the most important and frequently misunderstood aspects of Irish company formation, particularly for non-resident founders.

Minimum Number of Directors

An LTD requires at least one director. However, if there is only one director, a separate company secretary must be appointed. The director and the secretary cannot be the same person in a single director company.

EEA Residency Requirement After Brexit

Under Section 137 of the Companies Act 2014, at least one director of an Irish company must be ordinarily resident in an EEA member state. The EEA includes all EU countries plus Norway, Iceland, and Liechtenstein. Since January 2020, the UK has no longer been an EEA member. This change has significant practical implications for UK-founded businesses.

The requirement is about ordinary residence, not nationality. An Irish citizen who is ordinarily resident in the UK does not satisfy the requirement. Equally, a non-Irish EU citizen who is ordinarily resident in an EEA state does satisfy it.

The Section 137 Bond Explained

Where no EEA resident director is appointed, the company can still be incorporated but must first obtain a Section 137 non-resident director bond. This is an insurance product provided by authorised insurers in Ireland. The bond is essentially a guarantee that the company will fulfil its obligations under Irish company law and tax legislation.

The bond is valid for two years and typically costs between 1,500 and 2,000 euros. It must be renewed every two years for as long as the company has no EEA resident director. The existence of the bond is noted in the incorporation documents filed with the CRO but does not appear as a public liability on the company’s balance sheet.

It is worth noting that the bond is not a substitute for good governance. The company still needs to maintain proper records, file returns on time, and comply with all applicable legislation.

Director Disqualification

A person who is disqualified from acting as a director in any EU member state cannot act as a director of an Irish company. The CRO checks against the CORE disqualification register. Undischarged bankrupts and certain categories of convicted offenders are also restricted from acting as directors.

Auto Enrolment Pension Obligations from January 2026

Ireland’s Auto Enrolment pension scheme came into effect in January 2026. Employers are now required to automatically enrol eligible employees into a workplace pension scheme. Employees aged between 23 and 60 who earn more than 20,000 euros per year and are not already members of an occupational pension scheme must be enrolled. Employer contributions start at 1.5% of the employee’s gross earnings in Year 1, rising to 3% in Years 4 to 6, and reaching 6% from Year 10 onwards. Employees contribute matching amounts and the state contributes an additional top up. For companies that are just beginning to hire in Ireland, Auto Enrolment needs to be factored into payroll planning from day one.

Irish Corporate Tax: Complete 2026 Breakdown

Tax is often the primary motivation for choosing Ireland as a business location. Here is a thorough explanation of the Irish corporate tax regime as it stands in 2026.

The 12.5% Trading Rate

The 12.5% rate applies to profits from active trading activities. Trading means carrying on a business of selling goods or providing services. The distinction between trading and non-trading income is important: if your Irish company holds investments, collects rent from property, or earns royalties from IP held passively, those receipts are taxed at 25%.

To benefit fully from the 12.5% rate, it is also essential that the company is genuinely managed and controlled from Ireland. Revenue and the courts assess central management and control by looking at where the board meets, where key strategic decisions are made, and where the company’s real business activities occur. A letterbox company with no real substance in Ireland risks being denied Irish tax residency or challenged on its access to treaty benefits.

The 25% Rate on Passive Income

Passive and non-trading income is taxed at 25%. This includes income from property, loans, investments, and certain categories of royalty income that do not qualify for the Knowledge Development Box. If your business model involves significant passive income, you should take specific tax advice on how to structure the Irish entity to minimise exposure to the higher rate.

R&D Tax Credit at 35%

The R&D tax credit allows companies to claim back 35% of qualifying research and development expenditure. Qualifying activities include systematic investigation, pure research, applied research, and experimental development. The credit applies to both revenue expenditure (salaries, materials, consumables) and certain capital expenditure. Companies that have no taxable profits can claim the credit as a cash refund from Revenue over a three-year period, making it directly valuable to startups and pre-revenue companies.

Knowledge Development Box at 6.25%

The KDB provides an effective tax rate of 6.25% on profits derived from qualifying IP assets, including patents, copyrighted software, and certain computer programs developed through R&D activity conducted in Ireland. The KDB rate is essentially the 12.5% trading rate halved, achieved through a tax deduction equal to half of the qualifying IP profit. To qualify for the KDB, the R&D that generated the IP must have been carried out (at least in part) by employees in Ireland.

Capital Gains Tax

Capital Gains Tax is charged at 33% on gains arising from the disposal of chargeable assets. For companies, this applies to gains on the sale of property, investments, and certain other assets. However, a substantial participation exemption is available for gains arising on the disposal of qualifying shareholdings. Where a company holds at least 5% of the ordinary shares in a trading subsidiary and has held that stake for at least 12 months, the gain on disposal may be exempt from CGT under certain conditions. This makes Ireland an attractive location for holding company structures.

VAT in Ireland

Ireland’s standard VAT rate is 23%. A reduced rate of 13.5% applies to construction, property services, certain fuels, and some agricultural inputs. A reduced rate of 9% applies to certain tourism and hospitality services, newspapers, and sporting facilities. Businesses with a turnover above the registration thresholds (42,500 euros for services, 85,000 euros for goods) must register for VAT. Voluntary registration is beneficial for businesses that incur significant VAT on their costs and wish to reclaim input tax.

Ireland and the OECD Pillar Two Global Minimum Tax

From 1 January 2024, Ireland implemented the OECD Pillar Two global minimum tax rules. These rules require large multinational groups with global consolidated revenues of 750 million euros or more to pay a minimum effective tax rate of 15% in each jurisdiction where they operate. For groups that fall within scope, the Qualified Domestic Minimum Top-up Tax (QDMTT) applies in Ireland. For the vast majority of small and medium sized businesses incorporating in Ireland, Pillar Two is not relevant. However, any group approaching the 750 million euro revenue threshold should seek specialist advice before incorporating.

Summary of Irish tax rates applicable in 2026

| Tax Type | Rate | Applies To |

| Corporation Tax on Trading Income | 12.5% | Active trading profits for all companies |

| Corporation Tax on Passive Income | 25% | Investment income, rental income, passive royalties |

| Pillar Two Minimum Rate | 15% | Groups with global revenue above 750 million euros |

| R&D Tax Credit | 35% | Qualifying research and development expenditure |

| Knowledge Development Box | 6.25% effective | Profits from qualifying IP assets |

| Capital Gains Tax | 33% | Gains on asset disposals; participation exemption available |

| VAT (Standard Rate) | 23% | Most goods and services |

| VAT (Reduced Rate) | 13.5% | Construction, certain fuels, some services |

| VAT (Reduced Rate) | 9% | Hospitality, newspapers, sporting facilities |

Ongoing Compliance Obligations

Incorporating a company is just the beginning. Irish companies have a clear and recurring set of compliance obligations. Missing deadlines, particularly the Annual Return, can result in financial penalties, loss of audit exemption, and ultimately the involuntary strike off of the company from the CRO register.

Annual Return (Form B1)

Every Irish company must file an Annual Return with the CRO each year. The first Annual Return is due within 6 months of the company’s date of incorporation. Subsequent Annual Returns are due on the Annual Return Date (ARD), which is typically set 12 months after the previous ARD. The Annual Return must be accompanied by the company’s financial statements for all companies other than those availing of a late first return exemption.

Late filing of the Annual Return attracts a late filing fee of 100 euros, increasing by 3 euros per day up to a maximum of 1,200 euros. More significantly, a company that files its Annual Return late loses its entitlement to audit exemption for the following two financial years, potentially adding thousands of euros in annual audit costs.

Annual Financial Statements

Companies must prepare annual financial statements (profit and loss account and balance sheet) in accordance with Irish GAAP or IFRS. These must be filed with the CRO as part of the Annual Return, normally within 9 months of the company’s financial year-end. Small companies that meet at least 2 of the following 3 criteria may claim audit exemption: annual turnover of less than 12 million euros, balance sheet total of less than 6 million euros, and fewer than 50 employees. Audit exemption reduces the compliance cost significantly for smaller operations.

Annual General Meeting (AGM)

An Irish company must hold its first Annual General Meeting within 18 months of incorporation. Subsequent AGMs must be held at least once every 15 months and within 9 months of the company’s financial year-end. Single-member companies can pass resolutions in writing and may not need to hold a physical AGM, but the requirement should be confirmed with the company secretary.

Corporation Tax Return

The corporation tax return must be filed with Revenue within 9 months of the company’s accounting year end. For companies with accounting periods ending on 31 December, this means the return (and payment of any balance of tax due) is due by 23 September of the following year (for companies filing online). Preliminary tax is payable earlier in the year: small companies (with a prior year tax liability below 200,000 euros) pay preliminary tax by the 23rd of the month before the year-end.

RBO Updates

Any change in the beneficial ownership of the company must be notified to the RBO within 30 days of the change occurring. This includes changes arising from share transfers, the issue of new shares, or changes in the control structure of a corporate shareholder. Failure to update the RBO is a criminal offence under Irish law.

PAYE and Payroll Obligations

If the company pays any salary or benefit in kind to an employee or director, it must operate PAYE withholding tax, PRSI (Pay Related Social Insurance), and USC (Universal Social Charge) through the Irish payroll system. Real time reporting is required: employers must submit payroll information to Revenue on or before each payroll payment date using Revenue’s online PAYE Modernisation system.

VAT Returns

VAT registered companies must file periodic VAT returns with Revenue. The frequency depends on the company’s annual VAT liability. Companies with a VAT liability above 3,000 euros per month file monthly. Those with liabilities between 14,400 and 36,000 euros per year file bi monthly. Smaller businesses may file bi annually or even annually. Returns and payments are submitted through the ROS portal.

Costs of Setting Up a Company in Ireland in 2026

Here is a realistic cost breakdown for an Irish company formation in 2026. Costs vary depending on whether you use a formation agent, whether you need a Section 137 bond, and the ongoing complexity of your business.

| Cost Item | DIY Minimum | Via Formation Agent | Notes |

| CRO registration fee | 50 euros | Included in package | 25 euros for online only constitution |

| Formation agent fee | Not applicable | 250 to 600 euros | Varies by service level |

| Section 137 bond (if required) | 1,500 to 2,000 euros | 1,500 to 2,000 euros | Required if no EEA resident director |

| Nominee EEA director (annual) | Not applicable | 500 to 1,500 euros/year | Alternative to the bond |

| Registered office address | 200 to 500 euros/year | 200 to 500 euros/year | Virtual office in Dublin |

| Tax registration (TR2) | Free via ROS | Included in most packages | Corporation Tax, VAT, PAYE |

| Company secretarial (annual) | 500 to 1,000 euros | 500 to 1,500 euros | Annual Return, minutes, records |

| Annual accounting and compliance | 1,500 to 3,000 euros | 2,000 to 5,000 euros plus | Depends on turnover and complexity |

| Business bank account | Free (digital) to 10 euros/month (traditional bank) | Same | Digital accounts free; banks vary |

For a typical non-resident LTD with no EEA director, using a formation agent, a virtual registered office, and professional accounting support, expect total first-year costs of approximately 5,000 to 8,000 euros. This includes the Section 137 bond, registered office, formation fees, and basic annual compliance. Costs rise with complexity, headcount, and turnover.

Business Banking in Ireland: What to Expect

Opening a business bank account is one of the practical steps that founders often underestimate in terms of time and documentation. Ireland’s banking sector comprises traditional banks, challenger banks, and licensed electronic money institutions. Each has different strengths and requirements.

Traditional Banks: AIB and Bank of Ireland

Allied Irish Banks (AIB) and Bank of Ireland are the two largest retail and business banks in Ireland. Both offer comprehensive business current accounts, credit facilities, merchant services, foreign exchange, and relationship banking support. For established businesses or those seeking lending, a relationship with a traditional bank is valuable.

The application process for traditional banks typically takes between 2 and 6 weeks. Both banks conduct thorough Know Your Customer (KYC) and Anti Money Laundering (AML) checks. Most branches require at least one director to attend an in person meeting to open the account, which presents a logistical challenge for non resident founders. You can request an appointment at a Dublin branch and combine it with a business visit to Ireland if needed.

Documentation required typically includes: Certificate of Incorporation, Company Constitution, evidence of registration with Revenue (tax registration certificate), RBO confirmation, certified copies of identification and proof of address for all directors and beneficial owners, and a business plan or description of expected activities and transactions.

Digital Banking: Revolut Business, Wise Business, and Stripe

For early stage companies, particularly those that operate online or internationally, digital banking providers offer a fast and practical alternative. Revolut Business and Wise Business both accept Irish registered companies and complete their onboarding entirely online. Account opening typically takes between 24 and 72 hours. Both platforms offer multi currency accounts, international transfers, virtual and physical cards, and expense management tools.

Digital providers do not offer lending, overdraft facilities, or credit cards in the traditional sense. They are best suited to companies that need fast access to a working account rather than a banking relationship. Many companies start with Revolut Business or Wise for operational purposes and open a traditional bank account alongside it as the business grows.

Common Mistakes to Avoid When Setting Up in Ireland

The Irish company formation process is generally smooth, but some recurring mistakes cause delays, penalties, and in some cases, high additional costs. Here are the most important ones to avoid.

- Assuming UK residents still qualify as EEA directors. Since Brexit took effect on 31 January 2020, UK residents no longer satisfy the Section 137 EEA residency requirement. This is the single most common mistake made by UK-founded businesses. Always confirm the residency status of proposed directors before filing.

- Missing the first Annual Return deadline. The first Annual Return is due within 6 months of the date of incorporation, not the end of the first financial year. Many new founders confuse these two dates. Missing this deadline results in financial penalties and the loss of audit exemption for two years.

- Delaying RBO registration. Most Irish banks will not open a business account until the company can provide evidence of RBO registration. RBO registration should be completed within the first few weeks of incorporation, not left until it becomes an obstacle.

- Failing to register separately for Corporation Tax. CRO incorporation and Revenue tax registration are completely separate processes. Receiving your Certificate of Incorporation does not mean you are registered for Corporation Tax. File your TR2 form within 30 days of commencing activity.

- Using a PO box as the registered address. A PO box does not satisfy the legal requirement for a registered office address. The address must be a physical location in Ireland where documents can be served. A virtual office address provided by a reputable company is perfectly acceptable.

- Conducting board meetings outside Ireland. If the company’s central management and control is demonstrably located outside Ireland, the company may not be treated as Irish tax resident by Revenue. Key board decisions should be made at meetings held in Ireland. Minutes should record the location of each meeting.

- Overlooking the Auto Enrolment obligations from January 2026. Employers who fail to enrol eligible employees in the Auto Enrolment pension scheme face penalties. If you are hiring in Ireland, confirm your obligations with your payroll provider or accountant from the outset.

- Not maintaining statutory registers. Irish companies are required to maintain registers of members, directors, secretaries, and beneficial owners. These must be kept at the registered office and must be up to date at all times. Failure to maintain statutory registers is an offence under the Companies Act 2014.

How UCI Ltd Can Help You Incorporate in Ireland

Setting up a company in Ireland involves multiple interdependent steps. Getting any of them wrong, such as submitting an inconsistent Form A1, using the wrong registered address, or omitting required identity documentation, leads to rejection by the CRO and delays of several weeks. UCI Ltd specialises in Irish company formation for domestic and international clients and manages the entire process on your behalf.

What UCI Handles

- Company name availability check via the CRO CORE portal and name reservation

- Preparation of Form A1, Company Constitution, and Form VIF for all directors

- Section 137 non-resident director bond arrangement, where required

- Provision of a nominee EEA resident director service where required

- Submission of all documents to the CRO and management of the incorporation process

- Receipt of the Certificate of Incorporation and Company Registration Number

- Filing of the TR2 form with Revenue for Corporation Tax, VAT, and PAYE registration

- RBO registration for all beneficial owners

- Provision of a registered office address in Dublin

- Ongoing company secretarial services, including Annual Return filing, AGM support, and statutory register maintenance

Turnaround Times

Where all required information and documents are provided promptly, UCI targets the following turnaround times: CRO Certificate of Incorporation in 7 to 10 working days (standard) or 5 to 7 working days (expedited), Revenue tax registration within 3 to 5 working days of CRO approval, and RBO registration within 2 to 3 working days of receiving required beneficial owner documentation.

Why Use a Formation Agent?

While it is technically possible to complete CRO registration yourself, the practical reality is that errors in Form A1 or the Constitution are common and result in rejection and delay. Formation agents are familiar with the CRO’s specific requirements and the most frequent reasons for rejection. For non-resident founders in particular, having a professional based in Ireland managing the process removes a significant operational burden.

Conclusion

Ireland offers a genuinely compelling package for international businesses: the EU’s lowest corporate tax rate on trading income, full single market access, an English-speaking common law environment, an upgraded 35% R&D tax credit, and a fast, largely digital incorporation process. In 2026, these advantages are complemented by a mature professional services ecosystem and a growing network of technology, financial services, and pharmaceutical companies that make Ireland one of Europe’s most dynamic business environments.

The company formation process in Ireland is straightforward when approached correctly. An LTD can be incorporated in as little as 5 working days. With tax registration and RBO filing, most companies are fully operational within 10 to 15 working days. The key requirements, particularly the EEA director rule and the Section 137 bond for non resident founders, are manageable with the right guidance.

Whether you are a UK business seeking an EU base, a US technology company establishing your European headquarters, or an entrepreneur from outside the EEA looking to access the EU single market, Ireland deserves serious consideration as your chosen jurisdiction for company formation.

UCI Ltd is here to make the process fast, correct, and straightforward. Contact us today to begin your Irish company formation.